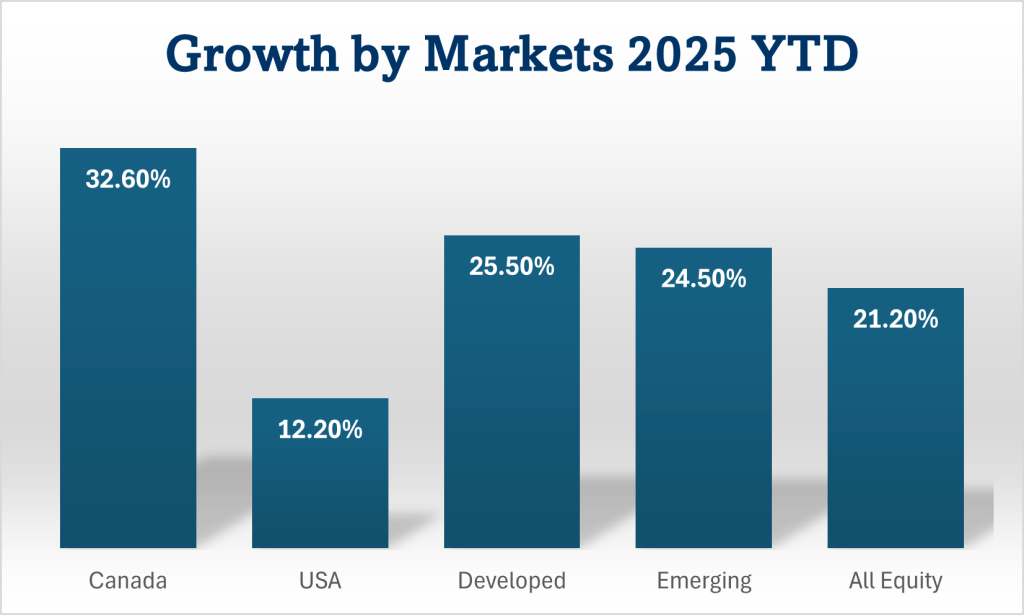

The big guy delivered some good days leading into the holiday. But even without the little Santa Claus rally at the end, 2025 was a great year for investors. Globally diversified investors were finally rewarded for investing outside the US markets. This time last year, who would have guessed that the Canadian market would have topped the performance charts?

Here’s what market performances around the world were like up to now in 2025 …

This chart is built by comparing popular broad market ETFs that trade in Toronto. All dividends & distributions are reinvested to maximise total return. The last column is one of the popular all-equity ETFs that are globally diversified. It hold chunks of all the other columns in this chart, with a serious overweight to the world’s biggest market, the US. And the Canadian market is also overweighted, especially compared to its size. Because we all love a bit of home country bias, eh! The US market has outperformed in recent years. Starting out, I would not have guessed that 2025 was going to be the year where it lagged. And it would have been an even bigger stretch to imagine that Canada was going to come out on top. As usual, the pundits & talking heads are all over which markets are going to do well next year. Is it possible they only get it right accidentally!?!

My prediction for 2026 is that I’ll probably be better off if I put any spare couch-cushion-cash I find into one of the all-in-one ETFs that matches my asset allocation goals. Of course, I am prone to thinking I know better from time to time. And while I can occasionally get lucky, I mostly screw up when doing my own stock, sector, or market picking! 🤪

Thank you for joining me here throughout the year, I guess we’re all done for 2025. And here’s hoping the world is a nicer, kinder place in 2026. May whatever light that lights your way shine ever brighter this holiday & beyond!

Best wishes,

Paul

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

Financial planning is based on estimates & projections. It’s educated & data-driven guesswork. The return projection numbers are so precise that they run to two decimal places. Reality is not that predictable! Planning projections for equities have been about 6.5%, give or take, for the past few years. On a year by year basis, it’s been way off. Markets have done far better. They could have done far worse. But the projections generally work well, when considering average returns, over longer timelines. After the exceptional market returns of the 90s, a financial plan using 6.5% for projections might have been considered too conservative. But a 50/50 mix of the US & Canada would have returned an average of almost 8% annually, from 2000 up to today. Looking back, that 6.5% wouldn’t have been a bad number to create a plan with in 1999, eh? But things can get crazy over shorter time horizons. Especially when retirement withdrawals come into play.

Grumpy old guys & gals who retired in the last 10 or 15 years complain about not being able to draw down their big RRIF accounts fast enough. Their portfolios are growing faster than they can spend them down. While many of these retirees are probably brilliant investors, some just got lucky! They timed the start date of their retirement pretty much perfectly. The 50:50 US & Canada portfolio would have returned almost 12% annually since 2010. Almost double that 6.5% planning number. Now there’s nothing wrong with being lucky. But luck is not always good enough for retirement planning.

That same 50:50 portfolio would only have returned a little more than 2% annually from 2000 to 2009. An investor who went all in on the American market over that decade would have had a negative return. The US market lost money over that 10 year period. And that’s without withdrawing any retirement income from it. The really big question with financial planning going forward, especially for new or imminent retirees, is this … what will the next few years be like? Those early retirement years can matter. A lot. As we saw above, average return numbers work really well over the long haul. But a severe or protracted downturn in early retirement, like the 2000 to 2009 period, can make a real mess of a plan. Taking a big hit immediately after retirement can seriously impair income for all the years that follow. The message here is that we cannot assume that the high returns of recent years will continue. Planning must allow for these different outcomes.

Financial planning guidelines have to thread a needle with respect for a wide range of potential returns. And it’s wise to err a little on the conservative side of what the long term data say. Many recent retirees, & new financial advisors, have not experienced something like the lost decade back in the early 2000s. To varying extents, we are all influenced by recency bias. And recently, things have been great. But we may need to temper the optimism & plan a little more cautiously for the future. Especially if retirement is imminent. Despite our retired friend’s success over the past 5 or 10 years, thinking we can begin retirement & spend at a consistent 10% rate is very risky.

So if planning is just guesswork, should we ignore it? Absolutely not! Nobody can foretell what happens next, but that makes having a plan even more critical. The purpose is to figure out how to best use our money so that we can pay the rent & buy groceries all the way to the end. Plans include success rate estimates & simulations that show if the plan can survive the best & the worst combinations of market cycles. Plans can include fun things like bucket list travel & fancy cars. Along with some things we hope aren’t needed, like illness or meeting long term care needs. It’s important to have a plan that considers the many vagaries of retirement. It’s equally important to have regular plan reviews & revisions over the years to ensure things stay on track.

Getting a financial plan done professionally can be very expensive. If you are paying an advisor to manage your retirement, financial planning may, indeed probably should, be included as part of that service. A good financial plan is a crucial part of living a successful retirement. Even for those DIY folk with a good knowledge of what’s required, having another set of eyes review the plan may still make sense. Indeed, it may be worth having a plan done by more than just one professional advisor. I know, sorry!

DIY folk tend to be frugal by nature & some may not want to pay for a professional plan. I get that. But you could ask about getting a review of your DIY plan, or a freebie, or a demo plan from whatever institution you have your money at. Some financial institutions provide that service. Sometimes you just need to ask. Fortunately, more & more planning tools are becoming available for the DIY cohort nowadays. Maybe with AI, we’ll even get some apps for that! But until that perfect app arrives, & perhaps even afterwards, getting a professional financial plan done might matter for most of us. Planning, especially for retirement spending, is quite complex. If you are not using a professional to put a plan together, there are some tools available that may help. Check out some of the tools in this post DIY Financial Planning … An Update. I have used the Adviice platform mentioned there & there are others like Optiml & MayRetire that I haven’t played with yet. Doing our own planning on a spreadsheet usually carries a greater risk of error. Whereas these platforms are getting feedback from a wider public audience, which helps weed out the errors & improve the product over time. Some of them have an access path to professional planning services. It’s great to see tools coming onto the market for DIY financial planning. As they improve & get smarter, perhaps they’ll help the profession space to offer more competitive services too. But until that happens, we’re stuck paying more. And despite the high price, it’s worth the spend if it helps us avoid a bad outcome.

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

Many years ago we visited some Italian friends for dinner. That was the first time I realised that pasta wasn’t meant to have a couple of pounds of stew heaped on top of it. Pasta in our house was usually over-boiled spaghetti, buried under lots of meaty-tomatoey stuff. Sometimes, we tossed in a few tablespoons of curry powder. Or maybe some jalapeños. And left-over spuds were always a no-brainer addition. Look, I’m not saying I didn’t enjoy some of these concoctions. But I was totally taken aback by how much I truly enjoyed the far simpler pasta that we experienced at our friends’ house. Portfolios are a bit like pasta in that respect. Sometimes, we can get carried away by having too many ingredients to choose from. Simpler can be better.

BlackRock’s iShares XGRO (20% fixed income) & XBAL (40% fixed income) have been available as all-in-one portfolio solutions since 2007. The arrival of the all-equity ETFs boosted interest in these off-the-shelf portfolios. In 2019, Vanguard Canada launched VEQT, their all-equity ETF. In that same year, the iShares XEQT ETF & Horizons (now Global X Canada) HEQT were also launched. And in 2022 we got BMO’s ZEQT. These funds are globally diversified, with about 45% of the allocation going to the US, 30% to Canada, & the remainder going to International, which includes a small allocation to emerging markets. These ETFs hold 10,000, or more, different company stocks from around the globe. That is some kind of diversification! And according to Harry Markowitz, a Nobel Prize-winning economist, diversification is the only free lunch in investing. There are a bunch of academic papers that support this level of diversification. While there are minor squabbles about percentages, or how great the American market is, I think some of us could benefit from using the allocation model employed by these highly diversified ETFs. Of course, that won’t stop us trying to mess with a good recipe from time to time, eh?

My own portfolio has gone through changes over the years. I was a growth investor at one time. Later, a dividend growth investor. Over time, new ETFs made it easier to chase the next hot sector or geography, so I started adding some of those. It wasn’t long before my portfolio looked more like one of my mad Irish-Indian-Mexican, & only vaguely Italian, pasta dishes! I finally got around to doing pasta the Italian way. It took me a little longer to learn how to apply that same keep-it-simple philosophy to my portfolio. But both cooking & investing are a little easier now. I will, however, admit that I occasionally toss a little hot pepper, or a little hot stock, into the recipe too!

Regardless of your preferred investment philosophy, there’s probably an all-in-one solution out there for you now. Along with the 100% equity ETFs, if you want 20% bonds, there are the V/X/ZGRO ETFs. The V/X/ZBAL ETFs cover the 40% bond allocation model. And so on. If you want the fund managers to take care of selling shares for you for income, BMO now has the T Series ETFs, like ZGRO-T & ZBAL-T. These ETFs dispense monthly income at the rate of 6% annualised. Now this distribution is well supported by recent market performance, but you should consult a professional to see if that 6% spending rate is sustainable throughout a lengthy retirement. Global X launched some funds for the high income investor. In 2023, EQCL provided a covered call & leveraged ETF that pays out at about a 12% rate. This sounds like a dream ETF &, since it was launched, it has been. Along with the fantastically high distribution, the underlying share price has continued to grow. But a 12% withdrawal rate might not be a safe bet for anyone starting out with a long retirement horizon. To complement this, Global X also have a globally diversified ETF with only covered calls. And another with only some leverage. What’s your favourite flavour?

With any fund that deviates from just holding & compounding plain old company stocks, it’s worth comparing its total return performance against an equivalent regular version. Regardless of huge differences in yield, total return comparisons offer a very useful perspective on relative performance. This is important to review during different parts of the market cycle. Many of these new funds look good, but they’ve only been active during a period of generally great market growth. Or with some smaller shocks that recovered quickly. Comparisons of these newer funds over recent shorter timelines are not as useful. Be wary of overly optimistic expectations until there’s some history of performance during longer or more severe downturns. Maybe these funds will do well. But getting it wrong with overly optimistic expectations can wreak havoc with retirement planning.

So what’s the message here? Having a big, sloppy, messy set of investments can add work & stress to the job of managing a portfolio. It’s worth comparing such a portfolio to the far simpler portfolios like those asset allocation ETFs we talked about above. If you are confidently outperforming an equivalent all-in-one or asset allocation fund, & if you don’t mind the work, then carry on doing what you’re doing. But if the off-the-shelf ETF is beating your portfolio over the long haul, you might want to ask why. Could the simple recipe be worth considering?

Of course you absolutely should consult a professional before you start moving investments around. There are so many things that can go wrong. You don’t want to get hit with a big tax bill from selling off investments in a taxable account, for example. Nor from shifting things between tax sheltered or tax deferred accounts incorrectly. That’s a huge no-no. Professional assistance may be required to avoid these, & other, potential pitfalls. And finally, if a big, sloppy, messy portfolio is underperforming by a significant amount, it may even be worth paying a professional to manage things. DIY investing isn’t something we’ve sworn an oath of allegiance to! At the very least, it may be worth interviewing a few financial planners & advisors, to get a feel for what they might do differently for you. Even if you decide to continue with the DIY approach, these encounters can be very educational. They may even help you create a better plan. You’ve already got a financial plan though, right?

Okay enough with all that for now, can you guess what’s for dinner tonight! 😜

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

There are some simple tools that can help us figure out where we might stash some cash for a while. Preferably within registered accounts like the RRSP, RRIF, or TFSA. In a non-sheltered account, the tax exposure will negatively impact net returns, so factor that into the thought process. Regardless of the pros & cons of holding cash over the long haul, we can find ourselves wanting to sit on some cash from time to time. If the cash just sits there as cash, it’s under constant attack from inflation. The starting number remains the same. But the purchasing power is evaporating daily. Let’s see how that works.

Go to the Bank of Canada’s Inflation calculator & plug in $10,000.00, starting in 2014, & hit the calculate button. As of today, that returns a value of $13,108.11. That extra $3,108.11 is how much our original $10k would need to have earned in interest, in order to buy the exact same basket of goods in October 2025. If we were sitting in cash, earning nothing, we’ve lost almost a quarter of our buying power. The Bank of Canada rates are based on an average basket of consumer goods that track the consumer price index. We’re not average, of course, so our personal inflation rate might be different! Believe it or not, Statistics Canada can help with this. With the Personal Inflation Calculator! Here we can plug in the things we spend our money on & the calculator will give us our personal inflation rate, based on our individual spending biases. Don’t get all hung up on the finer detail of the results here, you just want some idea if you’re in the ballpark of the CPI numbers that the Bank of Canada produces. Depending on what you spend your money on, you may generally be a little higher or a little lower. Knowing that is sufficient for a reasonable comparison against the Bank’s data. For the purpose of this exercise, we’re going to assume we’re close to the Bank’s numbers.

On a side note: are you being bombarded by online advertising on short term promotional rates? I just saw one for a 4 month rate of 4.75% from a local credit union. Nice, eh? And hey, if you’ve got the time, & some cash sloshing around in a regular bank account, nothing wrong with hopping around to benefit from these offers. In regular accounts, be careful doing this with large chunks of money, where the yield might bump income into a higher tax bracket. Or into OAS clawback territory. In sheltered accounts, I prefer to avoid all the extra work required to chase interest yield. In these accounts, I like to keep it simple.

And the simple thing to do is to buy a HISA style ETF. There are many of them, so take your time finding one (or more) that you like. I’m going to use the Purpose High Interest Savings Fund, ticker PSA, for this example. It trades in Canada, in Canadian dollars, & it’s eligible for registered accounts. Today, the net yield (after MER is stripped out) is 2.44%. That’s an annualised number based on the rate for the past 7 days, so you can’t take it to the bank (🤪) for the long haul. But this yield number makes for an easy first-pass comparison to whatever else you might be looking at. There may be better rates out there on other ETFs, so do some hunting for comparison. But PSA is one of the older HISA types ETFs around & we can see what its total return is since 2014. And that’s why I used 2014 in the Bank of Canada example above.

If you had invested the same $10k in this fund when it launched, back at the end of 2013, it’d be worth $12,723.00 today. That is only 385 bucks shy of the inflation indexed number from the BoC calculator. After almost 12 years, that is a whole lot better than the $3,108.11 we’d have seen evaporate if we’d let the $10k sit in cash. By all means, shop around & see if can find something that suits you better. There are many HISA type ETFs on the market now, like CASH, HSAV, etc. There are also money market funds that provide a similar smooth line performance to the HISA ETFs, take a look at ZMMK, MNY, CMNY, by way of example. You can use the Interactive PerfCharts from StockCharts to do the comparison. While bond ETFs will usually outperform these cash type ETFs over the long haul, they are subject to greater volatility than the HISA & money market funds. I’ve included a couple of popular bond finds in the link so you can see how they compare. They may outperform over time, but people don’t like to sell shares of a bond ETF after a crash. And bond funds tend not to recover as well as equity funds do after a crash. The other thing to bear in mind here is that old investing adage: past performance is no guarantee of future results! But leaving money sitting in cash guarantees inflation erosion. Note – the link above has some of the ETF tickers already entered but the baseline time period is 200 days. Right click (or press & hold on a mobile device) the square at the bottom right of the chart where it shows “200 days” & select “All” from the menu that pops up. That’ll give you a longer timeline to look at.

Incidentally, owning a ladder of individual bonds is quite different to owning a bond fund. Buying individual bonds guarantees (for the most part!) that you’ll get your money back at the end of the term, along with getting the coupon payments en route. The mini-flash crash of some bond ETFs during 2020, & the bigger bond fund crash in 2022, have scared some investors into moving some of their hard-earned money into the more stable cash-like funds we are talking about here. You might need to talk to your financial advisor about how to balance across these products in your portfolio. But if you are going to hold some cash in interest bearing ETFs, some of these tools might help you evaluate your inflation exposure.

Purpose Investments Inc. also has a US currency fund – the Purpose US Cash Fund, ticker PSU.U. The current net yield on that is 4.03%, which could be useful if you have US dollars sitting around. And no, I am absolutely NOT suggesting that you go swapping your Canadian cash for US cash just to buy this for the better rate. There are a whole bunch of other considerations that surround currency exchange & conversion strategies. Learn how this all works before trying to play the currency game or it might cost more than it’s worth. But if you already have US cash sitting idle, an ETF like this might help offset the effects of inflation while it’s not being used.

I wish that interest rates could always be higher in our savings & investing accounts. While being almost nothing on our car loans & mortgages! 😜

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

It’s been almost a year & a half since the post entitled DIY Financial Planning … Is it for You? went up. I have learned a little more about the whole process since then. The biggest lesson is that financial planning is pretty complex & winging it is probably not a good idea. While financial planning is built on forecasts & estimates, it remains crucially important for retirement planning. We need to make a plan with the best estimates available. A plan provides a foundation. Something to work with & measure against going forward.

I continue to like using the Adviice platform to massage the data & predictions into a plan. This platform will not be for everyone. It does take time to learn. I sometimes worry about what might be missing. Starting out, I made errors that I only caught much later in the process. Though I used a pretty straightforward scenario, I still made mistakes & found myself wishing there was a do-over button on a number of occasions. I have to accept most of the responsibility for this. I should have watched a few of the instructional videos first!

It’s still just $9 a month but, now, you can convert to an even more frugally attractive $49 a year plan. For what you get, this is pretty amazing value. At this price, you get a lifetime of financial planning for what you might pay a professional for developing a one-time plan. Which is out of date when you walk out the door. A plan requires updating & tweaking periodically. Aside from the many changes that can impact our own lives directly, much financial planning is dependent on estimates. Although data driven, these inputs will change over time. Many professional planners, for example, use the projection guidelines published by sources like FP Canada™ & the Institute of Financial Planning. As does the Adviice platform. Now this is good information to plan with. Rather than a DIY investor thinking that the annualised 15% returns from the past decade or so will continue indefinitely into the future! While these projections are done by professionals (& they do put a lot of careful thought & work into this), it’s still just a set of best guesses. Reality will typically be different, either up or down, from the projections. These projections are updated annually. Ideally, we should be reviewing our financial plan following any major changes too. That might be the result of job loss, a health issue, an inheritance, a market crash, a lottery win, & who knows what else.

A retiree might benefit from an annual review, in order to confirm the spending plan for the next year or two. And maybe to confirm that the budget for the retirement home is still intact, should it be needed down the road. All that reviewing & confirming stuff can be more challenging if we need to pay a financial planner to do the reviewing & updating for us. Some of us can take a dismally frugal view of spending money on such things, right? I know it won’t be for everyone, but tools like Adviice can be part of the solution to that problem. With a bit of luck, AI will continue to to take on even more of the financial planning burden. These are complex tools & AI may enhance the usability, while adding some protective guardrails to help defend against our potential for errors.

In this regard, it can be very useful to consider what-if outcomes. Creating alternative scenarios in Adviice is now more comprehensive. For example, you can more easily look at the impact of the earlier demise of one spouse. Previously, you needed workarounds for this. Now you can just choose an age from one of the options in the AI cluster & hit recalculate. The low-cost, single-user version limits the user to one plan, but you can create up to 10 scenarios around that.

The platform does pretty much most of the things you’d expect. With many of these managed by making choices in the AI options. You can start OAS or CPP at different ages. And for each spouse. Set it to prioritise drawing down accounts in different order, beef up tax free savings accounts, limit OAS clawback potential, modify retirement spending up or down, smooth out taxes, manage the size of the after-tax estate you want to leave the kids, & more. Within each scenario, you can target something different. Just select & enable the appropriate options within the AI cluster. You can then use the “Compare” function to see the differences in outcomes between the scenarios. Along with a graphical representation of net worth, the columns of information for each scenario allow for fast & easy comparisons of all the useful information, like income, including CPP & OAS, taxes, lifetime withdrawals & spending, & so on. It’s all pretty cool.

It’s also interesting to colour outside the lines sometimes. You can build a scenario that cuts a portfolio’s value in half, for example. Then play with the AI cluster options to figure out how to survive that scenario. Since there are Monte Carlo simulations built in, you don’t need to do extreme things like this but, hey, it can be fun, terrifying, & educational! You can’t directly modify the FP Canada projection guidelines for returns in the baseline data, nor should we want to for the most part. However, there are workarounds to test with numbers worse, or better, than those guidelines. Create a new scenario & you can then make changes to the return metrics for each account under the “Advanced Options” button. Here you can bring down the returns to, for example, stress test a scenario where you think the guidelines might now be overly optimistic. Great options for those who like to play. And, after all that playing, you might end up with a plan. In fact several variations of a plan!

The easiest way to explore what’s possible is via the Adviice YouTube channel. You can also get more insight at the Adviice community on Reddit. Here, you’ll also get a good handle on how they respond as a company. They’ll acknowledging feature requests & partake in Q&A interactions that will give you a great feel for the user experience. They will also acknowledge where something is lacking & provide feedback on whether it’s being address in future releases. All pretty good & pretty transparent, I think. I have no affiliation but I am enthusiastic about the product & the company. For me, Adviice is a whole lot better than trying to create financial & retirement planning scenarios with my limited spreadsheet skills. Even with the Adviice platform, I don’t trust myself fully. I still might miss something important. So having a professional run a plan periodically is probably wise. A retirement plan is just too important a thing to allow for any unnecessary uncertainty or discomfort.

Inside the Adviice platform menu, you can actually book a review session with a real professional. One that can use the baseline plan that you created within Adviice. There are several advisors on board the platform, offering a range of services. These range from a review, all the way through to a comprehensive planning & support package. Some of the pricing is quite competitive, particularly for an oversight or review exercise. I don’t have any direct experience with these services, so you’ll have to assess this option further before making a decision on whether it might be right for you.

There are other new platforms coming into this space now. I haven’t played with them yet & I don’t know how they compare. But this is great news. Financial planning is so important & I know I wasn’t doing the greatest job with a spreadsheet. These tools can shed more light in the darker corners & that can make for a better plan. Potentially one a better outcome. These are the kind of tools that everyone needs access to. As AI improves, I’m looking forward to seeing them get smarter & easier to use. Hopefully this progress will deliver an even better product & at an affordable price. Easy to use, more idiot proof (I’m the idiot referred to here!), & affordable are key attributes. Many people are discouraged by the cost of a having a plan done by a professional, so affordability does matter. But costs aside, one thing is certain: we can all benefit from having a good plan. Especially one prepared far enough in advance to help us avoid going into a poorly planned retirement!

To sidestep from Adviice for a minute, I’ve also enjoyed playing with the TPAW Planner. This is a very interesting, & free, online planning tool that was developed by Dr. Ben Mathew. You can learn more about it on the Bogleheads thread for Total Portfolio Allocation and Withdrawal, that’s where the TPAW initials come from. This is based on the “lifecycle model” & it considers a variable withdrawal as a more appropriate strategy for retirement. There are a lot of Greek letters used in the formulae employed by the lifecycle model! The TPAW Planner, however, keeps all that under the hood & it is an easy tool to use. But you might not be getting all the detail you need either. It doesn’t get into taxation, all the registered account stuff, etc. so it’s not as all-embracing of detail like we’re used to seeing on Adviice, or on the financial planning video clips from the pros. It doesn’t cover all the bases that tools like Adviice & the other Canadian solutions do. But it might help provide another perspective of what things might look in retirement. It might be a good comparison exercise for any financial plan you might already have. Or to one you develop in Adviice or one of the other tools. TPAW Planner is pretty easy to use, but be sure to spend time reading up & understanding it, a lot, before trusting the results. There is a lot more to financial planning, & to this methodology, than first meets the eye. Simplicity can hide some of the dangers from sight. Even from experienced DIY planners.

Whatever you choose to do, even if it’s a spreadsheet or on a coffee stained napkin, a financial plan is hugely important. Unfortunately, sometimes we don’t know what we don’t know. If you don’t have the knowledge & confidence to do it yourself, keep yourself safe & pay for professional advice. We don’t want to discover we didn’t know something important when we’re half way through retirement, eh? Of course, the other challenge might be figuring out how to choose a good financial planner. That’s a whole other question but, at the very least, make sure they’re appropriately qualified & certified. Be careful out there!

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.