Short of having a stock picking crystal ball, most investors agree that diversification is a positive thing for our portfolios. We have old sayings like “don’t put all your eggs in one basket” to remind ourselves of the value of spreading risk around. We generally think that more is better when it comes to being diversified. But that depends on how you look at things.

Considering only the equity portion of our portfolio, we have some fantastic solutions in Canada with globally diversified all-equity ETFs. BMO has ZEQT, RBC iShares offers XEQT, & Vanguard Canada manages VEQT. Other Canadian institutions, including TD, Mackenzie, Fidelity, etc., all have their versions or something similar. Global X & others offer income-focused covered call & leveraged variants, with similar global diversity. BMO created their T Series ETFs for income seekers who prefer to avoid covered call & leverage strategies. Do your due diligence on whichever of these strategies might work best for you, but they are all globally diverse solutions. And that’s the real message here.

Any one of these funds provides something close to the maximum market-weighted diversity obtainable in the global public markets. It just doesn’t feel like that when you stick all your money into one ETF. If you’ve switched from stock picking to index investing, going from 50 stock holdings to just one ETF, then one lonely ticker symbol in a portfolio does not look like diversification, does it? But it is. For many investors, it may be the optimal way to get diversification. These funds are holding ten thousand companies, give or take, from all around the world. And here’s the kicker: buying any ETF that is less diversified than these ETFs actually reduces the balance of market-weighted diversification!

If you buy an additional financial ETF, for example, you are overweighting banks & financial institutions in your portfolio, relative to their respective market weights. All the holdings in any additional ETF are already contained in, & appropriately weighted in, the all-equity ETF solutions. Same if you buy a tech ETF. Or an ETF that would add weight to a region, such as Canada, the US, or international. If you disagree with the weightings in the all-equity ETFs, either by sector or geography, then by all means rebalance the weights by buying additional ETFs. But adding an extra ticker symbol to your holding by buying your favourite Canadian bank ETF does not increase the diversification offered by these all-equity funds. It just overweights stocks that were already correctly weighted in the single ETF solution. Despite how scary it might look, one might be enough. Rather than being a single basket, it’s more a basket of baskets. With about the right number of eggs in each of those baskets.

That said, there may be other elements of diversification to consider.

It may make sense to diversify with ETFs from more than one provider. The global stock exposure is approximately the same across most of these funds, but that’s not the diversification angle here. Who knows what might happen down the road, maybe a data center goes off line for our favourite fund provider. If some unimaginable thing happens, & we’re all in on that company’s ETF, we might be stuck redeeming those funds. Even if only temporarily. However unlikely that possibility, there might be a justification for holding very similar funds from other providers too. Splitting holdings across ZEQT & VEQT, for example, might be a reasonable thing to do.

Or, depending on the use for various accounts, it might be useful to hold similar funds, but with different strategies, across different accounts. Young investors, or retirees planning a legacy, might use a vanilla all-equity fund in the TFSA account, for example. While retired investors with an income bias might prefer to hold higher yielding variants that employ covered calls & leverage in a RRIF account. Still others might prefer the T Series type, like ZEQT-T, for income. Maybe even some of both. But you get the idea: it’s a mix & match thing. But this is for diversification by investing style across accounts with different goals. It’s not significantly diluting or changing the balance of the global diversification offered by any of the market-weighted solutions.

So by all means, go buy something different for fun, function, or fund manager diversification. Or by design, if you feel modifying sector or geographic allocations will suit your needs better. But be aware of what you’re doing if you’re only doing it because you just can’t bear to look at one or two ticker symbols in each account.

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

AI can be fun, eh? These days I use AI to touch up & modify my photographs in seconds. Ideas for a two week itinerary around Nova Scotia? AI can help. Need a recipe for dinner tonight? These bots can come up with answers to all kinds of questions. Of course, we don’t always like their answers. But some bots seem open to a little steering on some subjects. Pushing back on an AI response can steer them a little more towards our way of thinking. If we’re just looking for a digital buddy to agree with us, that’s great. If we’re looking for real guidance or real solutions, however, that’s maybe not so great. I wouldn’t bet the farm, or my retirement, on any AI advice just yet. Despite that, they’re still very useful. And a lot of fun to play with. I found a new way to play with my favorite AI buddies last week!

I was trying to solve an extreme Sudoku puzzle. After resetting the puzzle for the 3rd time, I thought I’d stuff it into some AI chatbots for assistance. I’d probably have got it done on the next attempt myself (😜), but this was a good opportunity to see what my digital pals would do. This was a just-for-fun comparison. It was less about solving the puzzle & more about insight into the personality traits of the chatbots that, I guessed, might struggle with this. In no particular order, here’s what the results feel like. Notice how I’m going with feelings here, instead of science!

I tossed in an image of the puzzle into Gemini &, within seconds, it confidently returned the solution. Along with a list of the key steps used to solve the puzzle. Only it wasn’t the solution. There were a couple of errors. After 10 attempts, the puzzle remained unsolved. But as the conversation rolled along, Gemini came across as somewhat sheepish, a little embarrassed even. And it sounded so apologetic, that I was sure it had some Canadian emotional training under the hood. Despite not getting to a solution, the experience was a bit like having coffee with a buddy that got it wrong. But you couldn’t help but love & admire the effort. Very pleasant to interact with.

Meta AI came back promptly with a solution too. But before I could point out that it was incorrect, it actually spotted the error itself & went back into problem solving mode. Same thing after the second incorrect solution was offered. Another couple of passes without a good solution had it come back to me with questions. Was it blaming me now for giving it a poor input!?! I called it out & asked it it was giving up. It took umbrage at that & went back to work! LOL Still couldn’t do it & it then suggested that the colours in the image might be distorting things. Rather than trust itself to figure out the numbers from the image, it wanted me to type in the numbers. With this enthusiastic bot, it’s tough to get a word in edgewise sometimes. I was too lazy to input the numbers it wanted, so that meant the puzzle wasn’t solved, but it was a reasonably friendly interaction. And another buddy I’d enjoy having a coffee with!

Grok talked some sciencey & solutions logic, while offering to help me with the steps necessary to solve the puzzle myself. When I asked it to go ahead & solve it for me, it began outputting solution after solution in an attempt to deliver the correct one. After several minutes of that, & dozens of grids, I gave up & shut it off. I love Grok from other interactions, but it’s hard to read any personality into this sudoku engagement. I deleted the chat in case the poor thing felt obliged to continue working on the problem in the background! Though afterwards I felt guilty that I didn’t check a few of the solutions along the way, I just assumed it knew it was getting it wrong, verifying that, & then trying again.

Deepseek had a go & got it wrong on the first pass too. Immediately proclaiming “Wait, that can’t be right”, before getting back to work to give it another try. It didn’t take long for it to get around to questioning the image quality. And whether I had provided all the necessary info. It got back to work after I confirmed it had all the available information. Then, almost in anticipation of another failure, it mentioned having to ignore colour & shading on my image. It subsequently got into telling me about the complexity, the logic, the use of pencils, & so on. Almost like it was entertaining me. while working away furiously in the background! After another failure, it asked me to confirm other details & it wanted me to do a little more work again. I had a feel for its personality by then, so I didn’t take the time for that. It was a nice, polite, & engaging interaction. Though not the jocular, back-slapping type, it is a friendly little bot & enjoyable to use.

Claude is another polite & friendly bot that tripped up with this puzzle. It went into a couple of autocorrect steps before quickly recognising it wasn’t going to solve the puzzle & it admitted that! Suggesting instead that I input the challenge to one of the dedicated AI sudoku solvers. In the real world, that’d be the right thing to do. If you don’t know the answer, say you don’t know, right? I can respect a bot that takes that approach too. I’ve just recently started using this one & I’m enjoying the interactions. It has a slightly different feel & I look forward to seeing how that plays out with other engagements.

Copilot came back with a friendly comment, but it couldn’t read the numbers & immediately asked me to input them. I like & use Copilot in many other ways, but this wasn’t what I wanted from the sudoku exercise so I abandoned that conversation. In general, Copilot has a friendly personality & I enjoy using it for a whole range of other activities & questions. It just didn’t work out with the sudoku image this time.

ChatGPT was the last one I tried. Unfortunately, I didn’t learn much about the bot’s personality from this interaction. Why? Because it took one quick look & returned the correct solution. Job done! However, I know from other interactions that this is generally a nice, polite & friendly bot too. Though I haven’t done this, you can even adjust its personality traits in your profile settings inside ChatGPT. While this has no bearing on how good the other bots are at any other activities, ChatGPT is the winner of this little sudoku challenge. Using the image I chose to input. And there’s not much science to my comparison, I was more interested in seeing how they reacted in the event they couldn’t solve the puzzle! Regardless of the brevity of this interaction, I generally enjoy using ChatGPT.

Just for fun, I went back to some of the other bots & told them that ChapGPT solved the puzzle at the first attempt! LOL

Gemini started its response to that with an “Ouch!” & some self-deprecating comments. But it was glad I got the solution from another bot & gave props for their win. Canadian, eh! All in all, a very nice human-like reaction. Meta AI figured that the competition just “parsed the starting digits cleaner” & asked that I type out the numbers for it next time. It felt like this bot was just a little grumpier about the outcome. But it did apologise for wasting my time & finished the conversation with a rah-rah “Let’s get it right” statement for the next time. I had already deleted the Grok conversation, so it didn’t get to add anything extra on the competitor’s win. Deepseek maintained its polite & friendly stance & apologised again for not interpreting the image well enough to provide the solution. And it offered to cross check the ChatGPT solution if I wanted to share it. Claude came back all friendly & polite again, even offering to build me a sudoku solver artifact for next time! It also acknowledged that it could be worth sticking with ChatGPT if it’s working for me. Pretty magnanimous suggestion that, eh? Finally, I felt Copilot was just a little snarky. It’s opening response was “Fair enough” when I told it of the competition’s success. Or maybe I’m just sensitive! After some other polite remarks, it restated that if I ever want to solve one properly that I should enter the numbers in a grid. The italics was from Copilot! This isn’t my perception of Copilot based on other interactions. Can a bot have a bad day!?!

All these bots are great to work & play with. Solving a sudoku puzzle from an image was just a fun comparison. They have a far wider range of capabilities. Each bot will have its own unique characteristics. Some features & capabilities may require a paid subscription. But even the free versions are wonderful tools for entertainment &, with added caution & due diligence, problem solving. They are going to become an increasingly bigger part of our lives & any excuse for learning more about them is worthwhile. So what did I learn from this little exercise?

While it’s fun comparing & contrasting these bots with different questions & challenges, I’m still wary of trusting the answers. Despite the feelings I imagine I’m experiencing as I interact with them, even they don’t pretend to have all the answers. In fact, they frequently encourage us to check alternative sources to validate their answers & suggestions. The danger is that these bots can sound very confident when answering. And they feel so personable sometimes. Real people can copy & paste, or modify, these AI answers. They too then can sound awfully confident. An added caution for when we are reading posts like this on social media.

I wonder how different a retirement plan might look from each of these guys!?! Sorry, from these tools, I mean. Tools for sure, but I can’t help but think that I’ll be giving some of them names before too long! LOL

PS … except for a few words & phrases in quotation marks, all of the above was written by an error-prone human. With feelings! Given that, you might want to cross check the information even more carefully! 😉

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

The growth investor needs capital appreciation & the sale of shares for income in retirement. The income investor wants an income stream that can be used for living expenses without selling shares. Until recently, dividend paying stocks were the primary solution for an equity income stream during retirement. But with modern dividend yields so low, that takes a large portfolio. Over the past 5 or 6 years, a flood of new high income ETFs have changed that picture. These new income funds use options strategies & leverage to generate far higher distributions than are available from dividends alone.

But do they work?

According to some retirees, the answer is yes. Critics of this income investing approach say these funds tend to lag an equivalent growth fund. For the most part, that’s true. But some retirees are living higher on the hog than they expected to because of these funds. And they’re posting pics from their sunshine destination vacations to prove it. They can do this because their portfolio distributions run anywhere from 5 to 15%, with some far higher even.

To be fair, given the phenomenal market performance of the past decade & a half, a growth investor could also have spent far more than the traditional 4% Rule allows for. Investing in an S&P 500™ fund, from 2010 onward, could have delivered an inflation-adjusted withdrawal rate of about 12% all the way up to today. The great market performance of recent years makes the 4% Rule look a little outdated, eh? But there’s no guarantee that will continue! Of course most retirees would probably not be in a 100% equity portfolio. Instead they would have invested in the more common 60/40 balanced portfolio. And that portfolio would not have survived that 12% withdrawal rate from 2010 up to today.

Now this is where it gets interesting with income investors. Because they seem to have a bias towards a higher equity allocation. Some are 100% invested in equity income funds. While very few professional advisors would recommend a 100% equity portfolio for a retiree, these new income focused retirees seem to be less troubled about relying on an all equity solution.

So how does that impact the retirement picture?

I’m going to use ETFs from Global X by way of example, because they have globally diversified all-equity portfolios that serve all the strategies we’ve mentioned. Ticker HEQT is a regular growth ETF. EQCC is the same thing with covered calls. While EQCL employs option strategies & leverage. For further comparison, Global X also offers HBAL, a balanced 60/40 portfolio that we can use to represent a more traditional retirement mix. At the time of writing, the yield data below come from each fund’s web page. Be sure to check at each fund’s web page for current data.

It is very important to recognise that this comparison timeline is far too short to be very useful for assessing how funds like these might operate under a greater variety of market conditions, & over a longer time horizon. However, the characteristics displayed are in accord with what you’ll hear in some of the online arguments.

The all-equity HEQT is the best performer for total return. The traditional 40% fixed income allocation of HBAL makes for the poorest performance here, as the bond allocation drags down the total return during times of great market growth. Also as expected, EQCC delivers great income, but at the expense of some of the upside. In this example, over this very short time, the covered call version does outperform the traditional 60/40 portfolio. Finally, the leverage added to EQCL adds back some of the lost covered call upside, though not quite enough to catch back up to the returns of the vanilla all-equity fund. Note that the total return column is with all distributions reinvested.

From a pure numbers perspective, the total return of the regular all-equity fund comes out ahead. Regardless of how the income stream is delivered, total return is always important. The growth investor would typically concentrate on the ‘Total Return’ column & claim the win for HEQT. The income investor might look at the income column & favour the income streams from EQCL or EQCC. It’s worth noting that all these ETFs, with all distributions removed, left a fund that continued to increase the NAV well ahead of the inflation rate. That’s not always the case with all such funds. But even with the high yield funds in this example, you could have spent all that income in 2025 & still grown the NAV!

But again be warned … that’s only over this very short timeline when markets have performed well.

Let’s return to that 100% equity allocation thing we mentioned earlier. All our high yield funds above outperformed the traditional balanced portfolio. Retired growth investors are more likely to have a fixed income or cash component. Moreover, most financial advisors will probably not recommend 100% equity portfolios for retirement, regardless of the investment approach. But retirees investing in these new income ETFs appear to be able to tolerate a higher equity allocation. And that behaviour means that they have outperformed the traditional balanced portfolio in this instance. Indeed some income investors abandoned the balanced approach in favour of their new income strategy.

That’s the crux of the strategy comparison dilemma. Sometimes, we’re not really comparing apples to apples. The first big question is this: should a retiree have an equity allocation of 100%? And if that 100% equity allocation can be justified, would you want to own the growth or the income style portfolio? The answer is, as usual, it depends!

There are studies that support a 100% equity portfolio through the accumulation years and throughout retirement. One of the most recent, & one of the most thorough, is Beyond the Status Quo: A Critical Assessment of Lifecycle Investment Advice, from July 2025 by Anarkulova, Cederburg, & O’Doherty. This paper is widely discussed amongst the gurus online, but even professional advisors seem reluctant to tell their older clients to jump on board an all-equity portfolio during retirement. However, if this proves to be correct going forward, then an income fund that only slightly (& I’m not sure how to accurately define ‘slightly’ here!) underperforms an equivalent all-equity growth fund might be useful. After all, investing is both a mathematical & a behavioural exercise. If the higher income stream helps a retiree stay the course with a higher equity allocation, might that be a better solution for retirement?

I don’t know the answer to that one either. But it is fun to think about!

We don’t have enough history to understand how these income funds, & their income streams, might survive a more severe crash or a prolonged downturn yet. But I certainly look forward to seeing how things play out going forward. Let’s be real here, if a fund can deliver a 10% yield while growing the underlying NAV faster than inflation, who wouldn’t want a piece of that action, eh! In fact, if it came with inflation security, I’d probably take that bet with a far lower yield!

Unfortunately, I don’t think we can consistently predict such positive outcomes for these income funds. They have done very well in recent years. But their recent successes probably shouldn’t encourage others to retire too early. If your retirement plan was to work towards having a million-dollar portfolio supporting a 5% withdrawal rate, it might not be prudent to flip everything into a fund with a 10% yield & retire earlier with only a half-million-dollar portfolio today. Indeed, any strategy running at its limits won’t work very well if things turn bad. And, given a long enough retirement timeline, there will almost certainly be some bad times ahead. We need to plan our retirement accordingly. On top of those style deliberations, the 100% equity allocation has been part of the solution for some. But it remains an open question for others. We didn’t even get into the active versus passive conversation today! There really are a lot of moving parts to consider with all this. I wouldn’t be surprised to find some investors doing a mix of these strategies. As they tread water, waiting to see how things play out over time.

One last thing to consider is the impact of all this on financial planning exercises. We need to be careful about conflating distribution yield and total return. They are not the same thing. We cannot assume that high cashflows will remain intact for income funds, in the event that a market downturn severely draws down the underlying portfolio. And especially if that happens over longer periods of time. Even if the yield percentage remains high, the actual income stream in dollars could still be seriously reduced. I think sticking with FP Canada’s projection assumption guidelines for financial planning makes sense, regardless of the investing approach. But that’s a whole other conversation that we’ll save for another day. And maybe a downturn will provide the insights we need before I get round to it!

Meantime, wear your water wings in the deep end & take care out there!

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

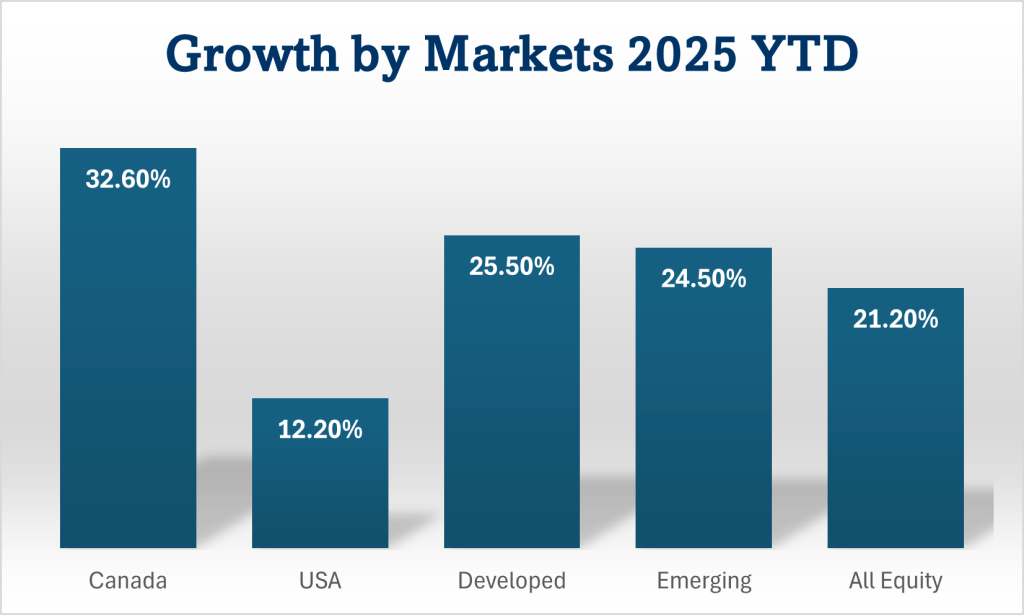

The big guy delivered some good days leading into the holiday. But even without the little Santa Claus rally at the end, 2025 was a great year for investors. Globally diversified investors were finally rewarded for investing outside the US markets. This time last year, who would have guessed that the Canadian market would have topped the performance charts?

Here’s what market performances around the world were like up to now in 2025 …

This chart is built by comparing popular broad market ETFs that trade in Toronto. All dividends & distributions are reinvested to maximise total return. The last column is one of the popular all-equity ETFs that are globally diversified. It hold chunks of all the other columns in this chart, with a serious overweight to the world’s biggest market, the US. And the Canadian market is also overweighted, especially compared to its size. Because we all love a bit of home country bias, eh! The US market has outperformed in recent years. Starting out, I would not have guessed that 2025 was going to be the year where it lagged. And it would have been an even bigger stretch to imagine that Canada was going to come out on top. As usual, the pundits & talking heads are all over which markets are going to do well next year. Is it possible they only get it right accidentally!?!

My prediction for 2026 is that I’ll probably be better off if I put any spare couch-cushion-cash I find into one of the all-in-one ETFs that matches my asset allocation goals. Of course, I am prone to thinking I know better from time to time. And while I can occasionally get lucky, I mostly screw up when doing my own stock, sector, or market picking! 🤪

Thank you for joining me here throughout the year, I guess we’re all done for 2025. And here’s hoping the world is a nicer, kinder place in 2026. May whatever light that lights your way shine ever brighter this holiday & beyond!

Best wishes,

Paul

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

Financial planning is based on estimates & projections. It’s educated & data-driven guesswork. The return projection numbers are so precise that they run to two decimal places. Reality is not that predictable! Planning projections for equities have been about 6.5%, give or take, for the past few years. On a year by year basis, it’s been way off. Markets have done far better. They could have done far worse. But the projections generally work well, when considering average returns, over longer timelines. After the exceptional market returns of the 90s, a financial plan using 6.5% for projections might have been considered too conservative. But a 50/50 mix of the US & Canada would have returned an average of almost 8% annually, from 2000 up to today. Looking back, that 6.5% wouldn’t have been a bad number to create a plan with in 1999, eh? But things can get crazy over shorter time horizons. Especially when retirement withdrawals come into play.

Grumpy old guys & gals who retired in the last 10 or 15 years complain about not being able to draw down their big RRIF accounts fast enough. Their portfolios are growing faster than they can spend them down. While many of these retirees are probably brilliant investors, some just got lucky! They timed the start date of their retirement pretty much perfectly. The 50:50 US & Canada portfolio would have returned almost 12% annually since 2010. Almost double that 6.5% planning number. Now there’s nothing wrong with being lucky. But luck is not always good enough for retirement planning.

That same 50:50 portfolio would only have returned a little more than 2% annually from 2000 to 2009. An investor who went all in on the American market over that decade would have had a negative return. The US market lost money over that 10 year period. And that’s without withdrawing any retirement income from it. The really big question with financial planning going forward, especially for new or imminent retirees, is this … what will the next few years be like? Those early retirement years can matter. A lot. As we saw above, average return numbers work really well over the long haul. But a severe or protracted downturn in early retirement, like the 2000 to 2009 period, can make a real mess of a plan. Taking a big hit immediately after retirement can seriously impair income for all the years that follow. The message here is that we cannot assume that the high returns of recent years will continue. Planning must allow for these different outcomes.

Financial planning guidelines have to thread a needle with respect for a wide range of potential returns. And it’s wise to err a little on the conservative side of what the long term data say. Many recent retirees, & new financial advisors, have not experienced something like the lost decade back in the early 2000s. To varying extents, we are all influenced by recency bias. And recently, things have been great. But we may need to temper the optimism & plan a little more cautiously for the future. Especially if retirement is imminent. Despite our retired friend’s success over the past 5 or 10 years, thinking we can begin retirement & spend at a consistent 10% rate is very risky.

So if planning is just guesswork, should we ignore it? Absolutely not! Nobody can foretell what happens next, but that makes having a plan even more critical. The purpose is to figure out how to best use our money so that we can pay the rent & buy groceries all the way to the end. Plans include success rate estimates & simulations that show if the plan can survive the best & the worst combinations of market cycles. Plans can include fun things like bucket list travel & fancy cars. Along with some things we hope aren’t needed, like illness or meeting long term care needs. It’s important to have a plan that considers the many vagaries of retirement. It’s equally important to have regular plan reviews & revisions over the years to ensure things stay on track.

Getting a financial plan done professionally can be very expensive. If you are paying an advisor to manage your retirement, financial planning may, indeed probably should, be included as part of that service. A good financial plan is a crucial part of living a successful retirement. Even for those DIY folk with a good knowledge of what’s required, having another set of eyes review the plan may still make sense. Indeed, it may be worth having a plan done by more than just one professional advisor. I know, sorry!

DIY folk tend to be frugal by nature & some may not want to pay for a professional plan. I get that. But you could ask about getting a review of your DIY plan, or a freebie, or a demo plan from whatever institution you have your money at. Some financial institutions provide that service. Sometimes you just need to ask. Fortunately, more & more planning tools are becoming available for the DIY cohort nowadays. Maybe with AI, we’ll even get some apps for that! But until that perfect app arrives, & perhaps even afterwards, getting a professional financial plan done might matter for most of us. Planning, especially for retirement spending, is quite complex. If you are not using a professional to put a plan together, there are some tools available that may help. Check out some of the tools in this post DIY Financial Planning … An Update. I have used the Adviice platform mentioned there & there are others like Optiml & MayRetire that I haven’t played with yet. Doing our own planning on a spreadsheet usually carries a greater risk of error. Whereas these platforms are getting feedback from a wider public audience, which helps weed out the errors & improve the product over time. Some of them have an access path to professional planning services. It’s great to see tools coming onto the market for DIY financial planning. As they improve & get smarter, perhaps they’ll help the profession space to offer more competitive services too. But until that happens, we’re stuck paying more. And despite the high price, it’s worth the spend if it helps us avoid a bad outcome.

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.