We needed to choose some wall & floor tiles when we bought our last new house. The builder worked with a local tile shop & we were sent there to make our selections. We spent several hours driving ourselves nuts. We were totally frustrated & depressed when we left. After three hours, the staff were relieved to see us go. And we still hadn’t chosen anything! Worse, we’d left the store in a mess. Tiles were spread across half the showroom floor. There were so many to choose from, we just couldn’t make up our minds. I called the store next morning & asked them to lay out about a dozen choices that were mainly black & charcoal. We went back & made our selections from the samples laid out. And we were on our way within ten minutes. Job done. Once we’d decided on a general colour theme, limiting the choices made it far easier to choose.

Investing can be a bit like that for new investors. There are too many choices. Should you invest in stocks or ETFs? For just about all beginning investors, the better choice is ETFs. But, on the Canadian exchange, I think there are more ETFs than stocks now. So which ETFs should you invest in? There are actively managed funds & those that passively track market indices or broad markets. Since, after fees, most professionals can’t beat broad market & index funds, most of the time, the correct answer for most of us is broad market or index funds. Now you are down to the black & charcoal tile scenario! All you’ve got left to do now is figure out which market funds to go with. Fortunately, the fund providers have made this easy for us these days. Not only have they reduced the selection of tiles we need to look at, they’ve put them all in one shopping cart for us.

Many fund providers in Canada offer a globally diversified basket of market index funds that cover the US, Canadian, developed, & emerging markets. The big three providers in Canada, Blackrock, BMO, & Vanguard, offer XEQT, ZEQT, & VEQT, respectively, for this very purpose. You still have to choose one. But the good news is that it doesn’t matter which one you choose, they’re virtually identical. If you want to feel better about it, choose one for your TFSA & a different one in your RRSP. Draw your choices out of a hat, if you like. You are now invested in broad market index funds across the globe. Make your initial investment in these funds & continue to add to them with every paycheque. Job done!

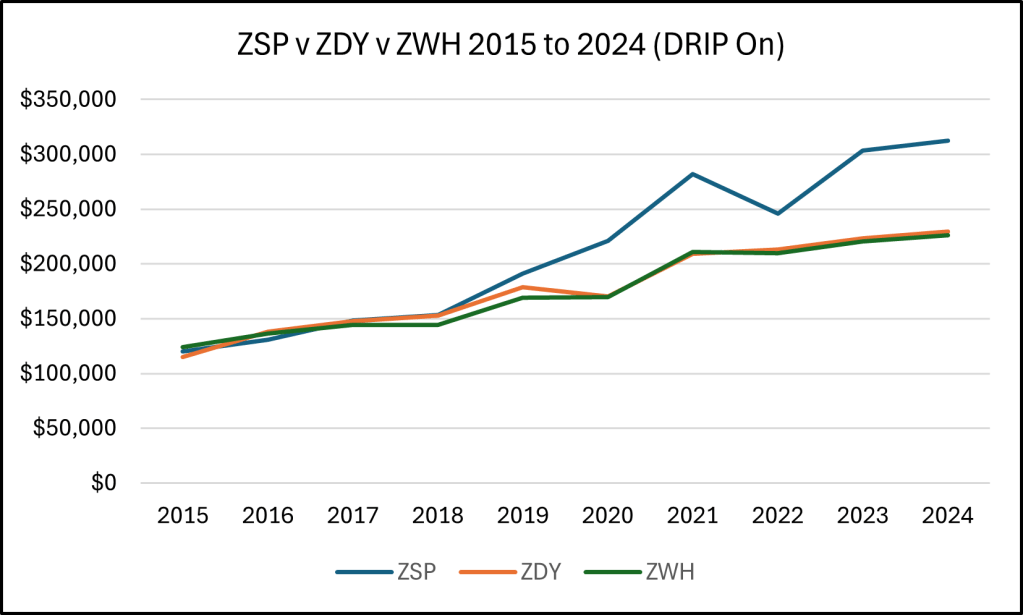

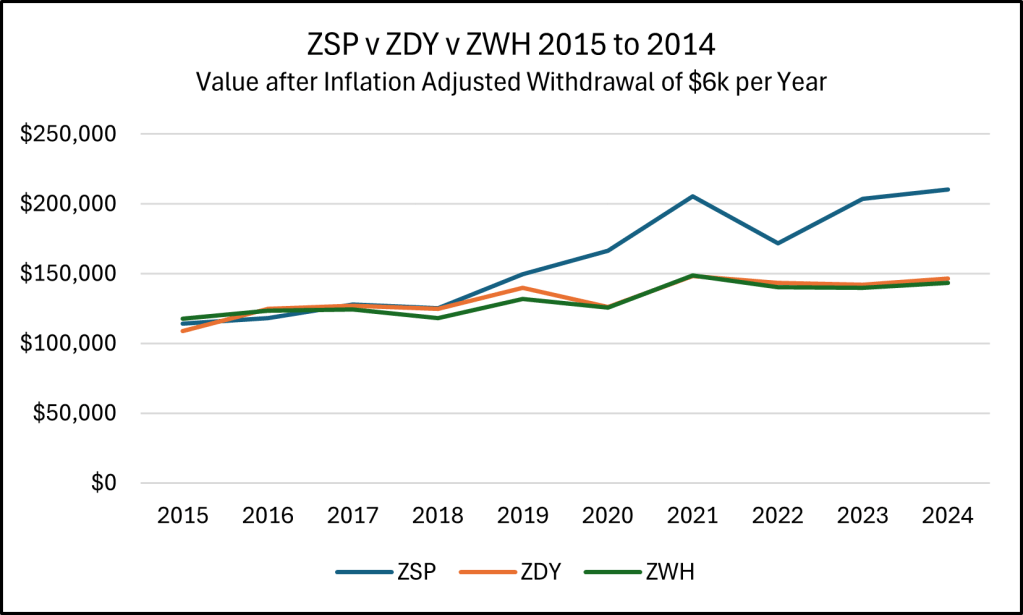

The online noise might suggest you do something differently. For example, the S&P 500® funds, like Vanguard’s VFV, have done phenomenally well for the past decade or more. The American market has crushed the competition. Investors are drawn towards whatever is doing well. That drives the price up. To be fair, there are worse things you could do than get into the US market. AI has a lot of allure these days, for example. However, it is worth remembering the lessons of history. If you’d invested in an S&P 500® fund back in 2000, you’d find yourself with about the same amount in your portfolio after ten years. Yes, today’s hot index created no wealth for a full decade back then. While the Canadian index about doubled over that same period. The Japanese market tumbled from its all time high in 1989. It took 34 years to get back to that high. Even “good” broad market indices can sometimes hurt if you take a narrow focus. Especially over shorter timelines. These global equity funds have all the markets. Including an overweight to the American market. You’re not missing out on what the American market offers, you are just diversifying more. The American market may continue to outperform. But that is still a narrow bet, with an uncertain outcome. Warren Buffett has the confidence & skill to go in harder on more winners than losers. And he loves the American market. But he tends to think in far longer investing timelines than the rest of us. These equity funds are globally diversifed. Diversification is considered the only free lunch in the investing world. And this global approach is a good investing appetiser for a novice investor.

Look, you might not shoot the lights out with one of the above funds. Or at least, not quickly. But you might have a decent chance of growing your wealth over time. Start out this way until you learn more. And when you learn more, you might even decide this is still the best approach for you. Trying to pick the winners, either stocks or narrowly focused ETFs, or trying to pick next year’s winning market, depends more on luck. And good luck with that!

If you invest in one of these funds, & if you continue to add to your investment with a little piece of every paycheque, you’re still not out of the woods. Because your investment will tumble anyway. It’ll go down 5% regularly, but it can also crash 10 or 20%, from time to time. Maybe even 50% or more on rare occasions. What will you do when that happens? What you should do is keep on investing your regular contributions. Buying more of the good stuff when it’s on sale will help grow your long-term wealth even more. Those periodic tumbles are a natural part of the process. Investing is a long game. If you are 30 today, you have 35 years to go to retirement at 65. You might have another 30 years of retirement to get through. That’s a 65 year investing timeline. Historically, the longer the investing timeline, the lower the risk of loss. But the risk of volatility is always with us on the journey. And it’s tough to weather short-term volatility. That’ll be one of the most challenging lessons to learn along the way. While past performance has no bearing on what the future might hold, it’s all we’ve got to go on. Markets have always recovered & gone on to new highs. And if we ever reach a point where global markets fail to grow over time, we’ll have a whole other set of problems that our investments likely won’t fix. Instead of an emergency fund, we’ll need a farm in the wilderness!

Investing is tough, but these globally diversified funds make it easier to get started. And for young investors, getting started early is important. The best education comes from having something invested. And with these funds, you won’t be paralysed trying to choose something from everything available. Because you’ll have a little bit of everything in your shopping cart.

The tiles turned out great, btw!

If you want to learn more about saving & investing from the ground up, I’d like to suggest that you check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money