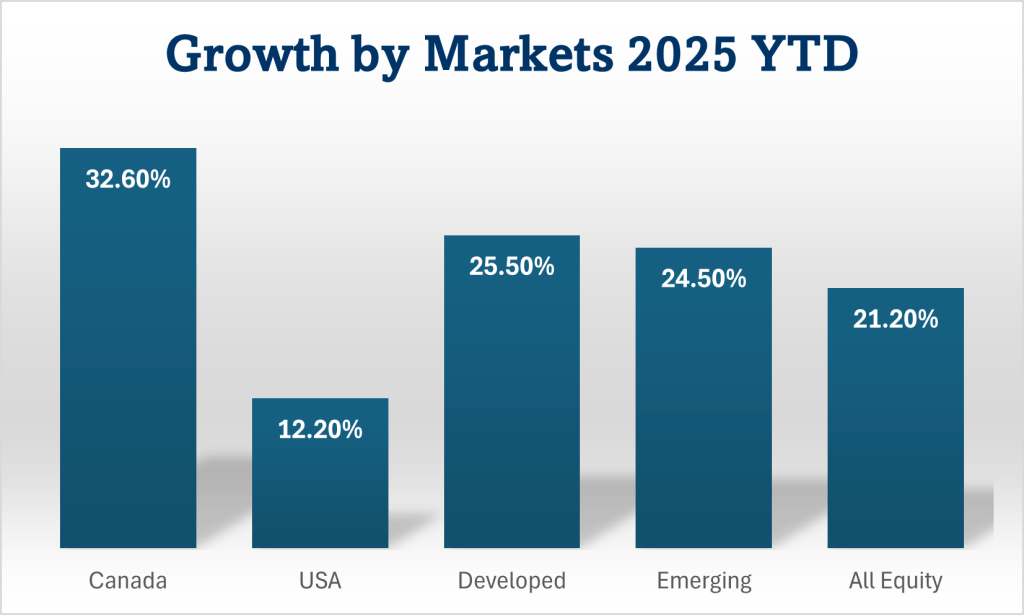

The big guy delivered some good days leading into the holiday. But even without the little Santa Claus rally at the end, 2025 was a great year for investors. Globally diversified investors were finally rewarded for investing outside the US markets. This time last year, who would have guessed that the Canadian market would have topped the performance charts?

Here’s what market performances around the world were like up to now in 2025 …

This chart is built by comparing popular broad market ETFs that trade in Toronto. All dividends & distributions are reinvested to maximise total return. The last column is one of the popular all-equity ETFs that are globally diversified. It hold chunks of all the other columns in this chart, with a serious overweight to the world’s biggest market, the US. And the Canadian market is also overweighted, especially compared to its size. Because we all love a bit of home country bias, eh! The US market has outperformed in recent years. Starting out, I would not have guessed that 2025 was going to be the year where it lagged. And it would have been an even bigger stretch to imagine that Canada was going to come out on top. As usual, the pundits & talking heads are all over which markets are going to do well next year. Is it possible they only get it right accidentally!?!

My prediction for 2026 is that I’ll probably be better off if I put any spare couch-cushion-cash I find into one of the all-in-one ETFs that matches my asset allocation goals. Of course, I am prone to thinking I know better from time to time. And while I can occasionally get lucky, I mostly screw up when doing my own stock, sector, or market picking! 🤪

Thank you for joining me here throughout the year, I guess we’re all done for 2025. And here’s hoping the world is a nicer, kinder place in 2026. May whatever light that lights your way shine ever brighter this holiday & beyond!

Best wishes,

Paul

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

A tidy portfolio can deliver growth or income with less work!

Managing a bag of stocks & ETFs is difficult. The fund companies have come up with products that have the potential to take away much of this pain. The all-equity ETFs & the all-in-one asset allocation ETFs offer a complete portfolio, wrapped in a single ticker symbol. Of course, no matter how good these products are, there might be some emotional investing needs too. Investing is both mathematical and psychological, eh? So maybe a little tweaking is okay!

Owning an ETF like BMO’s ZEQT (or iShares XEQT, VEQT from Vanguard Canada, etc.) is probably a good core choice for many investors. An ETF like this is already globally diversified. It’s geographically weighted according to market size & importance. It includes what many consider to be a reasonable home country bias. It holds large, mid, & small cap companies. It’s a really big haystack that I think Jack Bogle would approve of. According to Nobel Prize winning economist, Harry Markowitz, diversification is the only free lunch in investing. These funds meet that bar too. And finally, it’s a simple approach that is a lot less work for a DIY investor.

Do you spend your time figuring out if you should be dumping some of the tech ETF, so you can buy more of the gold one? Or trying to figure out when you should be selling the US market off, in order to buy Europe & Asia? Are you trying to work out what to do with this week’s hot & cold stocks? Worried about sector ETFs that might be going in, or out, of favour? Surging or failing markets? It’s all quite stressful & time consuming, eh? Life is too short. Especially as we get older! An ageing brain needs some challenge. But not torture. The globally diversified funds have everything in there. Some stuff will go up, some will go down. These funds are diversified & that’s how they work. And there’s one other important point to simplicity: if there’s a chance that the investing manager of a couple might depart first, a decluttered portfolio might be greatly appreciated by the surviving partner. The simpler the investing solution in place, the better it’s likely to be.

Want bonds? Choose one of the all-in-one ETFs (ZGRO, XBAL, VCNS, etc.) with a bond allocation that matches your needs. These are very simple solutions for highly diversified, asset-allocated portfolios, & they come with built-in rebalancing. Some investors might prefer an all-equity ETF that is complemented by separate bond & cash-like ETFs. There are some good arguments for breaking out the bond & cash allocations. It’s a little extra work, but it may make sense for some.

Now different investors have different approaches, so it’s not just about growth & accumulation. Fortunately, there is often a simple solution for many of the other investing styles too. For example, an income investor that favours high yield funds can choose something like the EQCL ETF, from Global X Canada, for the equity portion of their portfolio. It’s very similar in asset mix to the all-equity configuration of ZEQT. But instead of focusing on growth, this fund uses covered calls & leverage to drive a far higher distribution. People are different. Some are happy to go for maximum growth & sell off shares for income. Others prefer that the fund company delivers a bigger income stream for them. Rather than selling shares, these people are more comfortable figuring out how much of the big distribution they need to reinvest, in order to sustain & grow that income stream. Some investors like to mix & match such strategies. There are those who use different strategies in different accounts, so one style will be used in the TFSA & another in the RRSP. If you are new to these income funds, note that there are some total return & tax characteristics that are different to the regular type. Take the time to learn before diving in. Though that suggestion applies to everything. And it should have previously applied to the messy portfolios we sometimes find ourselves with! LOL

BMO offers yet another approach with their T6 Series ETFs. These funds dole out a targeted 6% distribution with funds like ZGRO.T & ZBAL.T. Here the fund manager is delivering the extra income, primarily via return of capital, but without the investor having to manage the sale of shares. This is cool for those who think that the 4% Rule isn’t allowing them to spend as much as they’d like. But it’s not as biased towards the far higher distributions that come from some of the high yield funds. This is more of a middle ground for income seekers. Don’t assume that this 6% distribution is a given for an inflation beating income stream for a full retirement lifecycle, by the way. Read this post on the Safe Withdrawal Rate in Retirement on why that might not work all the time. Nonetheless, the T6 funds will take care of automatically delivering a higher monthly yield, based on the value of the underlying fund at the end of the previous year. You still need to pay attention to the variability of the income stream over time. There may be a need to reinvest a little extra when income goes up after a great year, for example. That might safeguard against an income drop if the markets go down the following year. If the fund is subject to successive down years, the income stream will decline too. No solution is perfect when we try to predict the future, eh? But the bottom line is that simpler solutions exist for most investing styles & strategies. And for varying levels of distributions. Regardless of the investing strategy that is preferred, it shouldn’t stop an investor exploring ways to tidy up a messy & confusing portfolio. Especially if it reduces stress, while improving visibility & returns. Decluttering can be both refreshing & potentially rewarding.

If you can’t get your head around having so few holdings, how about putting the BMO one (ZEQT) in the RRSP, the iShares one (XEQT) in the TFSA, & Vanguard’s (VEQT) in the non-registered. Each one of these is globally diversified. They own a little piece of everything traded on the public markets. These are all essentially identical. But I get it. I totally feel the need to spread it around the different fund companies myself! There is also something to be said for making the single ticker solutions the core of a portfolio. While leaving a smaller allocation available for some gambling on the side. Sorry, I meant some intelligent macro investing on the side to boost alpha! If you know you can do it well, or if you can afford the greater uncertainty of return for a small part of the portfolio, then it might be fun, no it’s still crazy, okay! 😜

One other consideration. If the current messy portfolio performance is seriously lagging that of a single ticker solution, ask why. There may be good reasons why. And good reasons to justify staying the course with existing investments. But if we can’t come up with good answers (that aren’t guesswork or wishful thinking!), then consider this … if a portfolio is consistently underperforming the single ticker ETFs by an amount that is significantly more than 1%, it might be better off in the hands of an advisor who only charges 1% to manage the portfolio. Even if all the advisor does is invest it all into ZEQT or VBAL & manage the financial planning & cashflows for the investor thereafter!

There is also one big caution with all this. Decluttering a portfolio isn’t like spring cleaning at home. Do NOT rush into selling a bunch of stuff without getting some professional tax & investing advice. A long-term holding in a non-registered account, for example, may have significant capital gains tax liability if sold off. It might bump income up to a higher tax bracket. It might generate income that exceeds an OAS clawback limit, & so on. There are many potential issues, so seeking professional help is often the best course. There can be other challenges with balancing different fund types across the different account types. If you don’t know how to manage all this, get some help. Even if you’re just not sure if you know enough to manage all this, get some help first!

If you want to learn more about saving & investing, please check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

Good old-fashioned financial advice. But at what price?

DIY investing can drive you a little crazy. Do you like the crazy? Are you enjoying the work that comes with portfolio management? Some of us do! But it gets a little more challenging when we need to withdraw money during retirement. And will a surviving spouse be able to carry on with the crazy portfolio in the event the “money manager” departs first? Are you a good DIY investor? Or would you do better with an advisor?

There is an easy way to figure out if you should consider paying a fee to have a professional manage your portfolio & the retirement cashflow stream for you. And it’s this …

Compare your DIY portfolio performance against an equivalent ETF. We all need a “benchmark” to check our portfolio against. If you’re 100% in globally diversified stocks, for example, compare your portfolio performance to that of one of the XEQT, ZEQT, VEQT all-equity ETFs. If you’re in a 60/40 stock & fixed income mix, compare your DIY portfolio performance against XBAL, ZBAL, or VBAL. Are you buying a mix of Canadian & US large-cap stocks? Then compare that to an appropriately allocated portfolio of VFV & XIU ETFs. A portfolio filled with way too many stocks & ETFs might also be usefully compared against one of the all-in-ones. If your portfolio performance lags its benchmark by 1% or more, you might want to consider handing it over to a financial manager.

As an aside, since some of these all-in-one funds are so new, you may need to break them down into their constituent ETFs to usefully use them for benchmarking over longer time periods. The longer the history, the more useful the insights.

I’m using 1% here because many financial advisors charge an annual 1% of portfolio value as a fee for managing a portfolio. Is that fee worth it? Get the advisor’s performance history & compare that to an equivalent benchmark ETF too. Their recommended portfolio should only lag the return performance of those ETFs by the 1% fee. If they meet that requirement and if your self-managed portfolio was lagging by more than 1%, you could be getting better results by paying the advisor the 1% fee. As a bonus, you’ll have less work & an advisor who will tell you that everything will be okay when the markets are imploding. Hand-holding is included in their fee! For retirees, the advisor may also plan the income strategy & tax-efficiently manage the cashflow for you, across all accounts. You might even get some estate planning advice along the way. If you have a good advisor, they can deliver a lot of value. Even if they underperform the market average by the amount of the fee they charge.

Can you find an advisor that will consistently beat, after fees, the market or benchmark returns? I don’t know, but be sure to review their data supporting this opinion very carefully. And not necessarily against the benchmark provided by the advisor.

Unfortunately, it can be pretty challenging to tell if an advisor is any good. And those investors who are most challenged by DIY investing will also be challenged by the process of choosing a good advisor. We all like to believe we have the best doctor taking care of our health. In reality, most of them will be closer to average than exceptional. Fortunately, there are minimum standards & qualifications that we hope will ensure an adequate level of service from these professionals. The same is only variably true for financial advisors. Because the qualifications for calling yourself a financial advisor in Canada are variable. Some advisors are closer to being a product salesperson. And while some feel or profess a fiduciary responsibility, it is not a legal duty or obligation for many. They cannot just take your money & head off to a beach somewhere, but they may be putting their own, or their company’s, interests just slightly ahead of yours when it comes to investment choices. Even if only subconsciously.

Of course, a good salesperson will make you feel better about the relationship you are getting into. And that’s not a bad thing. But you also need an advisor who can at least deliver average market returns for a broadly diversified portfolio. Minus the fees. And you do need to know exactly how much you’re paying for whatever services & products are being recommended! There may be advisory fees and product fees, check carefully.

If you are a balanced 60/40 style investor, what would you think of paying an advisor to put all your money into ZBAL? Or maybe 60% into XEQT, with the other 40% into a couple of bond & HISA-type ETFs? We sometimes resent paying for simplicity. Advisors know this & are less likely to present you with such a simple portfolio solution. After all, if things are that simple, why would we need an advisor! Yet, in DIY mode, we sometimes struggle to follow the simple path ourselves. Instead, we prefer to work hard creating a portfolio that underperforms!

Of course, that simple solution might not be the ideal path for everyone. There may well be good reasons for some investors to pursue a lower volatility strategy, a higher income strategy, or whatever. But it is still useful to compare the total return on our own portfolios against those of low-cost, market index ETFs.

Robo-advisors are trying to bridge the gap between the advisory space & DIY, typically for about a 0.5% fee premium, in addition to ETF fees. I love the idea but it feels like you’re paying the added fee for the robo to pick the same ETFs that are in the all-in-one ETFs. Like some human services, they can fancy it up with one or two more esoteric picks. So you feel like you’re getting something extra for your money. But you generally won’t get the more valuable hand-holding that comes with the more expensive advisory services. Maybe AI will help with this down the road. But AI has been around for a lot longer than current market noise suggests & it hasn’t happened yet. Some robo-services do include human phone support. That might develop & grow into something more valuable going forward.

Isn’t there scope for fee reduction on the human advisory side too? Or for a service with a far more rapidly declining tiered fee-structure for larger portfolios? Are there any low-cost advisors out there? Shouldn’t there be more advisors competing with the 0.5% fees of the robo-advisors. Simpler portfolio advice & management should come with lower fees, no? I’m okay with portfolios constructed with low cost index funds. For some investors, the greater value may be more in managing asset location (what ETF goes in which account) & retirement cashflow. Some advisors include financial planning, a valuable service too. But can it be done for a 0.5% fee? Or less?

I realise that someone else’s job always looks easier than it really is from the outside. But I think financial advisory (& real estate) fees are very expensive in Canada. Particularly for the cookie-cutter portfolios offered by some companies. I’m totally okay with the right cookie-cutter portfolio, I just don’t want to pay through the nose for it. High fees are an ignorance premium being levied on a population that didn’t get this kind of knowledge coming through our educational system. And our schools still don’t prepare kids for the digital environment that now makes it far easier for the DIY investor to learn things the hard way. Fees will likely drop over time, as education & AI combine to work at improving the competitive landscape. Though in traditional Canadian fashion, it’ll probably drag out for a long time yet. And some of us older folk might not live long enough to benefit! 🤪

Regardless of the path we choose, it’s worth occasionally benchmarking our portfolio performance against a low-cost, well-diversified, ETF portfolio. One that approximately matches our portfolio’s asset allocation. Benchmarking can provide insight on how decent a job we’re doing with our investing strategy. And if we’re not doing such a good job ourselves, it may be worth talking to a financial advisor. But if you still find the idea of paying an advisor distasteful, then you’d better figure out how to learn to do it better on your own. Or maybe just use the benchmark ETFs instead!

If you want to learn more about saving & investing from the ground up, I’d like to suggest that you check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.

We needed to choose some wall & floor tiles when we bought our last new house. The builder worked with a local tile shop & we were sent there to make our selections. We spent several hours driving ourselves nuts. We were totally frustrated & depressed when we left. After three hours, the staff were relieved to see us go. And we still hadn’t chosen anything! Worse, we’d left the store in a mess. Tiles were spread across half the showroom floor. There were so many to choose from, we just couldn’t make up our minds. I called the store next morning & asked them to lay out about a dozen choices that were mainly black & charcoal. We went back & made our selections from the samples laid out. And we were on our way within ten minutes. Job done. Once we’d decided on a general colour theme, limiting the choices made it far easier to choose.

Investing can be a bit like that for new investors. There are too many choices. Should you invest in stocks or ETFs? For just about all beginning investors, the better choice is ETFs. But, on the Canadian exchange, I think there are more ETFs than stocks now. So which ETFs should you invest in? There are actively managed funds & those that passively track market indices or broad markets. Since, after fees, most professionals can’t beat broad market & index funds, most of the time, the correct answer for most of us is broad market or index funds. Now you are down to the black & charcoal tile scenario! All you’ve got left to do now is figure out which market funds to go with. Fortunately, the fund providers have made this easy for us these days. Not only have they reduced the selection of tiles we need to look at, they’ve put them all in one shopping cart for us.

Many fund providers in Canada offer a globally diversified basket of market index funds that cover the US, Canadian, developed, & emerging markets. The big three providers in Canada, Blackrock, BMO, & Vanguard, offer XEQT, ZEQT, & VEQT, respectively, for this very purpose. You still have to choose one. But the good news is that it doesn’t matter which one you choose, they’re virtually identical. If you want to feel better about it, choose one for your TFSA & a different one in your RRSP. Draw your choices out of a hat, if you like. You are now invested in broad market index funds across the globe. Make your initial investment in these funds & continue to add to them with every paycheque. Job done!

The online noise might suggest you do something differently. For example, the S&P 500® funds, like Vanguard’s VFV, have done phenomenally well for the past decade or more. The American market has crushed the competition. Investors are drawn towards whatever is doing well. That drives the price up. To be fair, there are worse things you could do than get into the US market. AI has a lot of allure these days, for example. However, it is worth remembering the lessons of history. If you’d invested in an S&P 500® fund back in 2000, you’d find yourself with about the same amount in your portfolio after ten years. Yes, today’s hot index created no wealth for a full decade back then. While the Canadian index about doubled over that same period. The Japanese market tumbled from its all time high in 1989. It took 34 years to get back to that high. Even “good” broad market indices can sometimes hurt if you take a narrow focus. Especially over shorter timelines. These global equity funds have all the markets. Including an overweight to the American market. You’re not missing out on what the American market offers, you are just diversifying more. The American market may continue to outperform. But that is still a narrow bet, with an uncertain outcome. Warren Buffett has the confidence & skill to go in harder on more winners than losers. And he loves the American market. But he tends to think in far longer investing timelines than the rest of us. These equity funds are globally diversifed. Diversification is considered the only free lunch in the investing world. And this global approach is a good investing appetiser for a novice investor.

Look, you might not shoot the lights out with one of the above funds. Or at least, not quickly. But you might have a decent chance of growing your wealth over time. Start out this way until you learn more. And when you learn more, you might even decide this is still the best approach for you. Trying to pick the winners, either stocks or narrowly focused ETFs, or trying to pick next year’s winning market, depends more on luck. And good luck with that!

If you invest in one of these funds, & if you continue to add to your investment with a little piece of every paycheque, you’re still not out of the woods. Because your investment will tumble anyway. It’ll go down 5% regularly, but it can also crash 10 or 20%, from time to time. Maybe even 50% or more on rare occasions. What will you do when that happens? What you should do is keep on investing your regular contributions. Buying more of the good stuff when it’s on sale will help grow your long-term wealth even more. Those periodic tumbles are a natural part of the process. Investing is a long game. If you are 30 today, you have 35 years to go to retirement at 65. You might have another 30 years of retirement to get through. That’s a 65 year investing timeline. Historically, the longer the investing timeline, the lower the risk of loss. But the risk of volatility is always with us on the journey. And it’s tough to weather short-term volatility. That’ll be one of the most challenging lessons to learn along the way. While past performance has no bearing on what the future might hold, it’s all we’ve got to go on. Markets have always recovered & gone on to new highs. And if we ever reach a point where global markets fail to grow over time, we’ll have a whole other set of problems that our investments likely won’t fix. Instead of an emergency fund, we’ll need a farm in the wilderness!

Investing is tough, but these globally diversified funds make it easier to get started. And for young investors, getting started early is important. The best education comes from having something invested. And with these funds, you won’t be paralysed trying to choose something from everything available. Because you’ll have a little bit of everything in your shopping cart.

The tiles turned out great, btw!

If you want to learn more about saving & investing from the ground up, I’d like to suggest that you check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money

Ever been in a lineup at the grocery store & switched to another line because it’s moving faster? Then the shopper ahead of you has their credit card declined! Most of us have done it, eh? And it’s a total crapshoot as to whether we win or lose. That makes it gambling. But it’s a gamble with little cost if we lose. And the elation of the occasional win makes it worthwhile. Many investors do the same thing, swapping stocks & funds based on which one is doing better recently. But when it comes to investing, we don’t always get to see the results right away. The reality is that reduced returns are more likely with this kind of behaviour. And this can have a negative impact on our financial well-being over the long haul.

There are few, if any, guarantees when it comes to investing. But chasing today’s hot stocks, sectors, ETFs, or markets usually results in underperformance. Today a growth strategy is the winner, next month it might be value, then it’s the turn of small caps, or emerging markets, & so on. But for most us, chasing what’s hot today usually doesn’t work that well.

For many DIY investors, a single, well-diversified fund or ETF is probably a better choice for the core of an investment portfolio. It might serve most of us well over a lifetime of investing. Buy that one fund & you buy everything at once. A young investor with an appropriate risk profile might go with one of the all equity funds like XEQT, VEQT, or ZEQT. An older or more risk-averse investor might choose one of the all-in-one funds that hold a bond allocation. The VGRO, XBAL, or ZCON (CNS) type funds from one of the big providers in Canada fit the bill here. Is one fund enough? These equity funds hold somewhere around 10,000 companies, from across the globe. Yes, that’s enough.

But, but, but … the S&P 500 Index has clobbered these funds recently. And the Nasdaq 100 Index has done even better. The American indices have outperformed most other county indices over long periods of time. So why might you do that boring global diversification thing? You do it because nobody knows what happens next. If we were having this conversation at the end of 1999 & you went all in on the S&P 500 Index, you could have turned $100k into about $104k by the end of 2010. A lousy compound annual growth rate of 0.35%. And that’s with all dividends & distributions reinvested along the way. Eventually it all came good & this index went on to ever greater highs. But would you have stayed invested for 11 years while the index did nothing? Meanwhile, if you put that same $100k in XIU, the iShares S&P/TSX 60 Index ETF, it would have grown to over $200k during that same period. Over that decade or so, the Canadian market trounced the American market. Had you gone all in on the Nasdaq back then, your $100k would be worth less than $62k by the end of 2010. This usually hot index went down. A lot. Could that happen again? I don’t know, do you? Do you feel comfortable going all in on the S&P 500 or the Nasdaq now? How about going all in on that hot stock that your buddy made a killing with?

Even younger investors might want to give the bond component a look, by the way. Yes, I know bonds are boring, old-person investments. And bonds got walloped in 2022, so who needs them, eh? But look at it from another perspective. The oldest bond ETF in Canada is XBB, the iShares Core Canadian Universe Bond Index ETF. It launched in 2000 so we’ll use the data from January 2001 to the end of 2010 for comparison. While the American indices languished, XIU turned $100k into more than $179k over this 10 year period. While this boring bond fund turned $100k into almost $176k. A boring bond fund almost matched the performance of the Canadian index & it dramatically outperformed the American indices during this decade. A bond allocation provides further diversification & this is another example of what diversification is all about. You probably won’t make a killing betting on all the horses in the race, but it might help you keep the shirt on your back!

It all boils down to this … nobody can tell the future. Nobody knows what happens next. And, when it comes to investing, the less you know the broader you go. When you don’t know, diversification can help moderate the effects of crazy fluctuations in one regional market or another. While a series of catastrophic events could drag down all markets globally, there’s a decent chance that some regional markets will hold up better than others. That doesn’t mean that a globally diversified portfolio, even one with a bond allocation, won’t go down, it will. But unless you know something that nobody else does, or unless you get lucky, you might do better by covering more of the bases. These globally diversified & all-in-one ETFs do that.

Now if you really want to play with something different, it might be fun to allocate a small percentage of your portfolio to one of the hot funds. Or even to whatever stocks you think are part of the next big thing. You may even win big with this allocation & then you’ll frown at the pedestrian performance of your globally diversified ETF. But the thing to remember is this: portfolio performance is measured over decades, not over mere months or even years. The results of your choices might not be apparent for 10, 20, or even more years. The caution in this tale is to be wary of allowing short term or recent performance having too big an influence on your longer term decisions. After due consideration, you may still choose to focus more on the American indices. Nothing wrong with that. But do it with your eyes open. And with an appreciation for how things might work over longer time horizons. Investing really isn’t like shopping, it’s a long game.

If you want to learn more about all this, & how to build a portfolio that might suit your needs better, read Double Double Your Money.

Happy Canada Day! 🇨🇦🍁🇨🇦

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinions are my own, so do your own due diligence & seek professional advice before investing your money.