As a Dad, I feel obliged to answer any of my kids’ questions as best I can. Naturally, I want my kids to think I’m a great Dad. But more often it’s because I don’t want them to make the same mistakes I did along the way. Recently, one of my kids asked me which version of the Vanguard S&P500® index funds they should buy. The choices were between VOO, on the US exchange, & VFV or VSP on the Toronto Stock Exchange. VFV is a Canadian dollar version of VOO. While VSP is the same thing, but currency hedged. I thought I knew the answer to this question.

The general comparison goes something like this …

Buying VOO from Canada incurs currency exchange fees. We need US$ to buy VOO. It’s not just the exchange rate, but we pay a fee for our brokerage to convert Canadian dollars to US dollars. You could try Norbert’s Gambit to reduce those costs. But there are still some added costs. Even with those costs, VOO should still outperform over time, since its expense ratio is 0.03%, compared to 0.09% for VFV & VSP. If VOO is held in an RRSP account, the American 15% withholding tax on the dividend is saved. Thanks to the tax treaty between the two countries. That does not work if you have American dividends being paid inside a Canadian ETF, like VFV or VSP. ETFs must pay the withholding tax. That’s two strikes against the Canadian ETFs. For a young investor, with a long investing horizon, going with VOO sounds like a no-brainer already, eh?

Investing outside an RRSP, both would suffer the withholding tax, but VOO would still have the lower fee advantage. Currency hedging, as with VSP, attempts to reduce the influence of currency exchange rate fluctuations between the US & Canadian dollars. Using currency hedging requires a little extra management, but the expense ratios of VFV & VSP are the same.

I was about to suggest that my kids learn how to do the Norbert’s Gambit thing & buy VOO inside an RRSP account. But I decided to run the numbers & compare all three.

This is what happened …

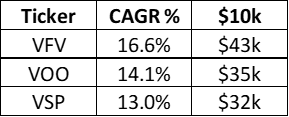

These are the results for a nominal $10k investment in each, made in November 2012. It’s important to note these are nominal dollar amounts for comparison, they do not take the different currencies into account. VFV returned at an annual rate of over 16%, while VOO was just over 14%. The currency-hedged VSP came in at an annual rate of 13%. Since VFV holds VOO, how could it possibly outperform VOO by that much?

To be perfectly honest, I would have done better putting some money into VSP back at the end of 2012, instead of some of the other choices I made! But, after looking at these numbers, what do you think I should suggest my kids do?

And why?

It wouldn’t be the first time I missed seeing the forest because of the tree pollen in my eye!