Which currency should we invest in, Canadian or US dollars?

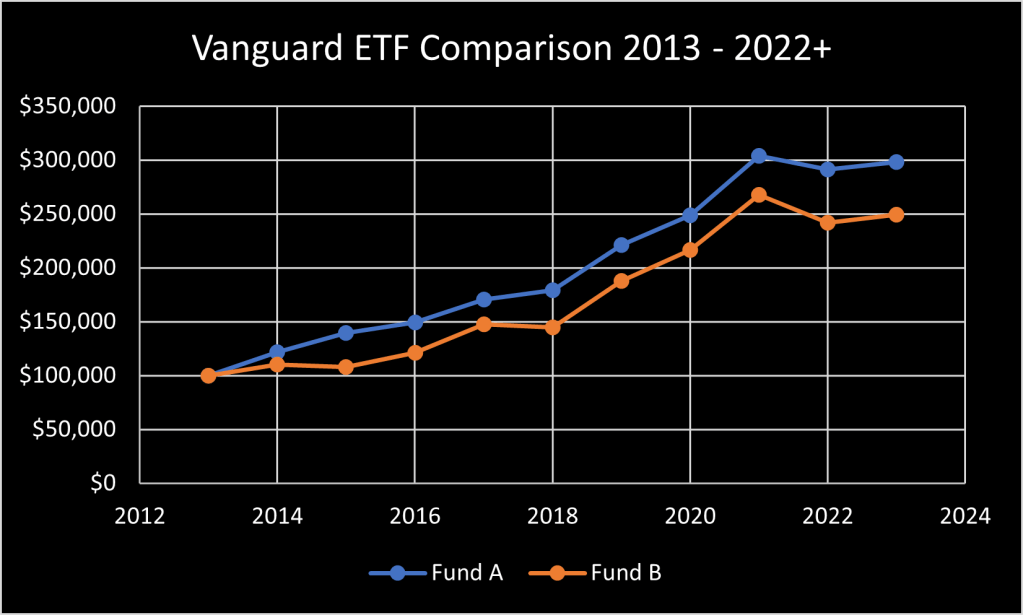

In this example, we’ll compare Vanguard’s US listed & US dollar denominated ETF (VOO), against the Canadian listed & Canadian dollar denominated equivalent (VFV) from Vanguard Canada. Imagine investing $10k back in 2012 in each of these ETFs. Conveniently, the Loonie & the greenback were approximately equal back then. One Canadian dollar was worth one US dollar. That means the $10k investment was of equal value, regardless of the currency.

With all dividends reinvested, here’s what the performance has looked like since then …

By March 2025, VOO grew from $10k to $52k, in American dollars. While VFV soared to about $73k, in Canadian dollars. VFV looks like the big winner. But it’s not.

Back then the currencies were at par. By the end of this chart, it costs $1.44 Canadian to buy one US dollar. If we sold off VFV at the end & converted the proceeds to US dollars, we’d have a bit less than $51k American. pretty close to the US dollar value of VOO. Similarly, if we sold all our VOO holdings & converted those US dollars to loonies, we’d have almost $75k Canadian. Bottom line is that they’re about the same. We’re only looking at about a fifteen hundred dollar (Canadian) difference in total return, with the American listed VOO coming out slightly ahead.

VOO should come out slightly ahead. There a few reasons for that, including the following …

1. It has the lower fund fee of 0.03%, compared to the 0.09% fee of VFV in Canada.

2. While it all happens inside the ETF, VFV loses a little of the dividend payout due to the 15% dividend withholding tax that the IRS (the US equivalent to the CRA) collects. This happens regardless of the account the Canadian listed ETF is held inside.

3. Though ETFs can do currency exchange at better rates than the typical DIY investor, there might be some additional currency exchange drag on VFV too.

If the fund fees were the same, if currency exchange didn’t have any fees, & if there were no dividend withholding taxes, the performance of the two ETFs would be practically identical. The apparent outperformance of VFV in the chart above is mainly due to the declining value of the Canadian dollar against the US dollar over that 12 year period. Both funds grew similarly in real value (as they should, since they both hold the same stocks). But VFV grew “extra” Canadian dollars over that time, in line with the increasing real value of the stocks inside the EFT. This compensated for the Canadian dollar falling in value against the US dollar. If the reverse had happened, & the Canadian dollar had gained strength against the US dollar over this time, VFV’s numbers would have lagged VOO on the chart. It would have “looked” worse. But, once you convert the currency in either direction, both would have looked pretty much the same again.

That said, there are some pros & cons with either choice.

If you have a bunch of US dollars already & you want to invest these greenbacks inside an RRSP account, VOO would be the better choice. It may not always be this way going forward but, under the current agreement between Canada & the US (& as it was over this timeline), the RRSP account shelters the investor from the dividend withholding tax that would otherwise apply to US based ETFs. On the flip side, if you don’t already have US dollars, you’ll have to pay currency conversion fees. Or learn the Norbert’s Gambit technique to minimise the currency conversion costs. If you want to avoid that currency conversion work, the outcome resulting from sticking with VFV is still pretty good. Particularly when investing outside a registered retirement account, where neither fund can avoid the withholding tax. That would bring the results a little closer together. It is worth noting that the bigger the investment, & the longer the time invested, the greater the potential impact. The $1,500 difference on this $10k investment example, would have been $15,000 on a 100k investment. You can do the math for a million dollar investment as your portfolio grows! And, for a more precise comparison, you’ll need to figure out the impact of currency exchange costs, back & forth, on the end result too.

I’ve ignored some other critically important tax wrinkles (there are some potentially significant exposures here) that come with foreign investing during the course of this comparison, so be sure to consult a tax specialist if you want to invest on exchanges outside of Canada. There are tax reporting requirements with the CRA above a certain value of foreign owned investments, for example. There are also potential IRS tax reporting requirements. And perhaps even US tax liabilities along the way. There’s a lot to learn. And if you don’t know, you’d be well advised to check with a professional advisor to help you figure out your US & foreign investing strategy. In addition, the outcomes may require the inclusion of more than just stocks, bonds, & ETFs. Any additional foreign property, like a holiday home outside Canada, for example, will impact your tax situation. Talk to an expert!

On the other hand, there is nothing wrong with investing in Canadian listed ETFs while you learn more about investing on foreign exchanges & in other currencies. It is a little less work to stick with the loonie. And the end result here was not too far behind the American equivalent. Many investors stick with Canadian listed ETFs, while still getting the necessary foreign exposure. There are also currency hedged ETFs that can help offset those currency fluctuations. But that’s a conversation for a another day.

Just remember that things would begin to reverse in the above chart, if the loonie were to gain in value against the US dollar going forward. In other words, VOO would then start looking better when charted against VFV. In the first 6 months of 2025, for example, VOO is up about 5%. While VFV is essentially flat. The real value of both is still close to the same. But the numbers are different due to a weakening US dollar this year, making VOO look better over this different timeline. This is more about how the numbers look, it’s not that the value is substantially different. Looks can be deceiving, eh!

If you want to learn more about saving & investing from the ground up, I’d like to suggest that you check out Double Double Your Money, available at your local Amazon store.

Important – this is not investing, tax or legal advice, it is for entertainment & conversation-provoking purposes only. Data may not be accurate. Check the current & historical data carefully at any company’s or provider’s website, particularly where a specific product, stock or fund is mentioned. Opinions are my own & I regularly get things wrong, so do your own due diligence & seek professional advice before investing your money.