The title is clickbait, please bear with me & I will try to redeem myself. If you do an internet search with that same title in the search box, what you’ll find is a series of links to pieces & papers that suggest exactly the opposite is true. Women, it turns out, are generally better investors than men. Guys seem to run on testosterone-addled brains that make them do silly things when it comes to investing. So women who are investing generally outperform men. However, this is not about which gender makes for a better investor. It’s about those women who are not saving & investing for their long-term financial security.

The challenge for women as group is that fewer women are investing, as a proportion of their gender population. Those women who are not saving & investing may have exposure to greater retirement challenges. Women are more likely to face poverty in retirement than men. There is a gender pension gap that results in a great number of women surviving on lower income in retirement.

Despite all the progress with gender equality over time, it’s just not enough. There are still glass ceilings that women butt up against in the workplace. Many companies pay women less than men for doing the same job. Some women are channeled into lower paid & temporary or part-time jobs. And women tend to be the ones that take career breaks to raise children. All these things lead to a lower lifetime income. And lower lifetime income can lead to a lower retirement income from savings & pension plans, including the Canada Pension Plan, for women. With women living longer than men, this only adds to their challenges for retirement. Women, on average, will need a bigger retirement nest-egg than a man, to take them through that longer retirement phase. And many women are not saving & investing enough, early enough, to counter that predicament.

While women continue to work on fixing all those other issues of inequality, saving & investing should be a priority from the earliest working years. Don’t trust your neanderthal male partner to do it for you. We’re not that good at it! This is one area where women can seize the advantage. By starting early. Given enough time, an early start can level the playing field.

Why do I care? Because my wife is likely to outlive me by, not just years, but decades. For some of us, the challenges only come to light much later in life. And I have kids, including a daughter. I’d like them to get started early too. I wish I’d known more in my younger years.

Unfortunately, the kind of people who are reading this stuff are probably already engaged & knowledgeable. You are likely already saving & investing towards a more secure financial future. But if you have friends who are not, please encourage them to start. Investing looks like a digital casino to those unfamiliar with it. But it doesn’t have to be. And, as I’m sure you know, it’s not so intimidating once you take the time to learn a little. Please share your knowledge with those who might benefit from it. And if you have kids, regardless of gender, help them get started on the path early. Unfortunately, the urgency to get started early only becomes obvious much later in life!

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinions are my own, so do your own due diligence & seek professional advice before investing your money.

According to the latest StatsCan data, from 2021, there are about 15 million of us that have TFSA accounts. There are about 30 million of us that are eligible to have TFSA accounts, so 50% of the adult population are not using this account. While some can’t afford to save & invest, there are still a lot of people missing out on what this account can do for them. TFSA means Tax-Free Savings Account.

Who doesn’t want something tax-free? If you have money sitting outside this account … WHY!?!

The other funny thing with TFSAs is that a lot of people are storing cash there. I know it says “Savings” right in the name, but parking cash is not what this account is about. Inflation evaporates the value of cash. Especially with today’s high inflation rate. There are no benefits to letting cash evaporate inside a TFSA. You need to invest in something. Even if you are worried about investing in the markets, you can put your money to work in a high interest tax-free savings account (HISA), in GICs, or in one of the cash savings or HISA type ETFs. Some of these are yielding 5% at the moment. You can harvest that 5% return in a TFSA totally tax-free.

Some of these choices are more liquid than others. Being “liquid” means you can convert whatever it’s in to cash right away. And that means you could consider storing some of your emergency fund inside a TFSA. A locked-in GIC, for example, is not suitable for an emergency fund. An emergency can’t wait for a GIC to mature. The bottom line is that it’s tough enough to save, whether it be for an emergency fund or a holiday fund, but reducing the value of those savings by not getting some kind of return is a waste. And not sheltering those returns from tax only adds to that.

I know some of you are are already way ahead of the game with this. But if you have people in your life that you even remotely care for, your friends, your parents, your kids, please teach them about the value of the TFSA. It’s too big a deal to miss out on. Sure they’ll have to learn how it works & what investments are suitable under different circumstances. But it is worth the effort. If they can’t learn enough to do it alone, encourage them to see an advisor for help.

If you are not filling up your TFSA with long-term investments, use the spare room for your spare cash. Let it work tax-free for you.

If you want to learn a whole lot more about how all this stuff works, read Double Double Your Money, available here on Amazon. If you have a Kindle Unlimited subscription, you can read it for free. If you don’t have a subscription, there is a current Amazon.ca promotion that gives you the first two months free, so you really can read it for free. Please read it & share the message. Help get it out to some of the other 15 million Canadians who are missing out on the tax sheltering power of the TFSA.

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinion are my own, do your own due diligence & seek professional advice before investing your money.

For a dividend investor, the answer is we never want to avoid dividends, right? After the last post on Canadian-listed American dividend ETFs, I thought I’d provide an alternative view to one that might have suggested dividend-growth investing is the way to go.

Dividend-growth investing is very popular. I’m a fan myself. Primarily because it is a strategy that can work reasonably well for an investor with limited skills & ability to assess the potential of a stock to provide good returns. Using fewer & simpler metrics than it takes to properly evaluate a stock, it’s possible for a DIY investor to choose a portfolio of dividend-growth stocks that can perform reasonably well. And, being focused on a growing income stream, rather than on a falling share price, can help some of us ride out market downturns. The other great attraction of dividends is that as a portfolio grows, the income stream can grow &, one day, it may even match the income stream from our day job. How cool would it be to have a portfolio that generates enough income to match your paycheque? Very cool, eh! A retiree with a portfolio that provides a 4% yield on retirement day, might look forward to never having to sell shares. Selling shares for income can be a traumatic challenge for some retirees. And if the income stream continues to grow more than inflation, our retirees golden years might truly be golden. There’s a lot of good to be said about a portfolio of dividend-growth stocks.

But, in the world of investing, things are never simple!

Picking the right dividend-growth stocks still takes a lot of work. And it takes additional work to monitor & maintain a portfolio of individual stocks. Dividend-growth may still be a valid strategy for some. But it’s worth back-testing your stock portfolio against a dividend-growth ETF portfolio every now & then. Just to see if all the extra work produced enough extra reward. Of course the yield from such ETFs often don’t match that of a portfolio of hand-picked dividend-growth stocks. We like our bigger dividends, eh! However, things can be different before & after retirement. And that raises some questions.

How many years ahead of retirement should we start building our dividend income stream? Does it make sense to start early & just let the DRIP work for us ahead of retirement day? Is it important for that income stream to grow before we retire? But the really big question is this: should we even be focused on an income stream ahead of retirement?

Let’s take a look …

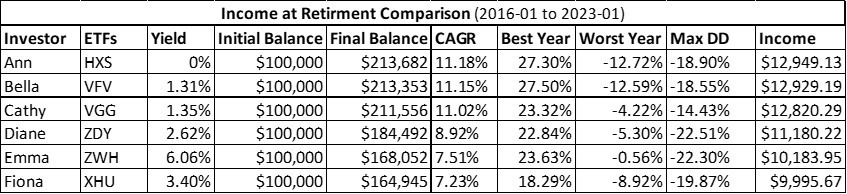

All our investors above put 100k into an ETF at the start of 2016, with a view to retiring at the end of January, 2023. Ann & Bella are oblivious to dividends. They both followed the market index investing philosophy & went with S&P 500 Index® funds for part of their US allocation. Ann chose Horizon’s HXS. This is a total return strategy that doesn’t pay any distribution. Unlike all the other ETFs, this one reinvests the value of the dividends inside the ETF. The income stream is zero. Bella went with Vanguard’s VFV index fund. In this, & all other cases, distributions were automatically reinvested (the DRIP) at no extra cost. Cathy likes the dividend-growth approach & invested in Vanguard’s VGG. She realised she might sacrifice some of the total return potential of the market, but she felt her choice was less volatile (it is, look at the Worst Year & Max DD columns) & that allowed her to sleep a little better. Dianne was lured by the higher dividend payout of BMO’s ZDY. This ETF has a pretty good history of share price appreciation & a decent dividend growth trend. She liked that. Emma wasn’t sure if she was into the whole FIRE thing yet but she thought that BMO’s ZWH might give her that option sooner. The juicy 6% yield from this ETF might make earlier retirement a reality for her. And the covered call strategy might offer some downside protection to boot. The Max DD is a little scary, but the worst year performance is the best of the bunch over this time period. Getting a good night’s sleep was important for Emma too. Fiona went with a more traditional dividend approach, going with the Blackrock’s iShares® XHU offering. This is an ETF that focuses on a basket of solid, reliable, higher yielding companies in the US. A good choice for an investor who favours this approach.

Looking at the Final Balance column, I’d be pretty happy if I’d thrown a few bucks into any of these ETFs back in 2016. But what is the point of this comparison?

It’s this …

Come retirement day, we will look at things differently. It’s not how much income was received & reinvested along the way. It’s not how much the income stream grew prior to retirement. It’s not about when we started to build an income stream. It’s going to be all about the value of the portfolio on retirement day. And how big an income stream that portfolio can buy to support our needs from that day forward.

Look at the Income column, the last one on the right. This is the income stream that would result from all the ETFs being sold off on retirement day to buy ZWH, the highest yielding ETF. The biggest income stream can be had by selling the portfolio that gave the best total return. And then buying the ETF with the greatest distribution, in this case ZWH. There is a 30% spread here, that’s significant. Notice that in most cases, the higher yielding funds tend to have lower total return over time. That might not always be the case & it might not be the case going forward. Not even amongst this batch of ETFs. Doing your own due diligence, as always, is important.

But, from a pure numbers perspective, it matters less what happens with dividends during the accumulation years. It only matters that the portfolio grows. As much as possible. The bigger the portfolio, the bigger an income stream it can buy on retirement day. In this example, how much the income stream grew during accumulation didn’t matter. Having a bigger yield on cost didn’t matter. The only thing that mattered was that a bigger portfolio bought a bigger income stream on retirement day. For simplicity & to maximise return, all investments were considered to be inside a tax-sheltered account. There are other implications, not covered here, for selecting ETFs like this in a non-sheltered account.

Emotionally & numerically, there are many reasons that investors choose to invest differently. Seeking solutions with lower volatility, the reassurance of a growing income stream, avoiding the need to sell shares, & so on, all factor in to individual choices. All these are all important considerations, for sure. But the message here is not that we all need to abandon our chosen strategy in favour of some other promoted strategy. It’s more about giving some thought to strategies that differ from our current path. Despite the reassurances we get from like-minded investors in our favourite social media groups, it can be useful to think differently about things from time to time. We shouldn’t fall in love with one particular strategy & block out all information that conflicts with that. It might be worth taking some time to learn about different perspectives & different strategies. Keep an open mind.

By the way, I’m not suggesting that you buy any of the ETFs here. Nor am I suggesting that everything gets dumped on retirement day for one high-yielding ETF. This is just an example to illustrate why we might want to think differently about our approach from time to time. It’s just as a valid to consider switching to a basket of individual, higher-yielding, dividend-growth stocks on retirement day, for example. Or sticking the proceeds into a portfolio of your favourite high-yield funds. Do whatever floats your boat for an income stream. Believe it or not, some will stick with the growth solution that got them there & sell shares for income. But regardless of approach you choose during the accumulation years, whatever you choose to do in retirement will probably work better with a bigger portfolio. 😜

So how do you accumulate?

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinion are my own, do your own due diligence & seek professional advice before investing your money.

If I lived in the US, I would probably split my US exposure between the Schwab US Dividend Equity ETF (SCHD) & the Vanguard Dividend Appreciation Index Fund ETF (VIG).

Why?

For a few reasons. The first is because I like dividend-growth stocks & both those ETFs focus on companies that have the potential to create a growing income stream. Dividend-growth companies appear to hold up better than growth stocks when the markets crash. Because I’m a bit of a chicken, I tend to I favour ETFs with lower volatility than the market. The goal of choosing lower volatility investments is to take away some of the market downside when bad things happen. When a conservative investor seeks to avoid volatility, what we really mean is that we don’t want our stuff to go down. We don’t mind volatility to the upside, of course! But lower volatility ETFs usually knock off some of the highs too. These two ETFs, however, are great performers. One slightly lags the market, while the other has a slight beat. Both provide that level of performance with less volatility than an S&P 500 Index® ETF. Since 2012, they had better annual performance than the market in the worst years & their biggest drawdowns were less severe than those of the market too. The bottom line is they have provided good performance over time. And they offer the potential for reduced anxiety during the bad times. My kind of investing.

While we can buy these ETFs in Canada, there are pros & cons to a Canadian investing through the US exchanges. Some combination of laziness, currency exchange costs, & a desire to avoid additional tax reporting headaches has many Canadian investors favouring Canadian-listed ETFs for their American exposure. Can we do that & get the results provided by ETFs like SCHD & VIG. Let’s take a look.

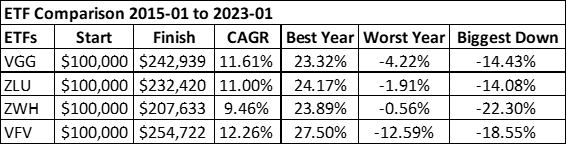

There are ETFs from all the big providers, like Blackrock®, BMO Global Asset Management, Vanguard Canada, Horizons & others, that provide US market exposure solutions for Canadians. In Canadian dollars. An easy choice for one of the contenders is the Vanguard US Dividend Appreciation Index ETF (VGG). This one is easy because it holds just VIG, the very same US ETF mentioned above. Of course, the expense ratio (fee) is higher in Canada, but we’re used to that, eh! I would like a Canadian-listed equivalent to SCHD, but there really isn’t anything doing exactly what SCHD does up here. BMO’s ZDY is vaguely similar but the BMO Low Volatility US Equity ETF (ZLU) looks interesting too. With all the online chatter about high yield ETFs in recent years, I had to include one of those for comparison & I went with the BMO US High Dividend Covered Call ETF (ZWH). I think this is one of the better ones in this space & it merits inclusion to see if all the talk about the downside protection that this strategy offers is really true.

Let’s cut to the chase …

For the market benchmark comparison, I’m using Vanguard Canada’s S&P 500 Index® ETF (VFV). With everything in Canadian dollars, the variable exchange rate noise doesn’t confuse the comparison. Here we see the results of 100k invested in each of the ETFs at the start of 2015. ZWH was launched in 2014 so the data (courtesy of portfoliovisualiser.com) for this comparison starts in 2015.

What do you think of those results?

As is often the case, the low-cost market index fund wins out for total return. Over a long lifetime of investing, that 1.26% difference between the annual returns from ZLU & VFV, for example, could be huge. If you can tolerate the volatility, Mr. Buffett’s advice is looking good, the low-cost market index fund is the winner. But for more fearful investors, the lower volatility choices might help keep them in the market during times of steep decline. Jumping in & out of the market in response to market fluctuations can be a wealth killer for investors. For that reason, my choices would be VGG & ZLU in this instance. They don’t come as close to market returns as the two American ETFs we looked at earlier. But they’re good enough for me & I think I’d manage a better night’s sleep with those in my portfolio. I must be honest here, I was taken aback by how well ZLU has performed over the past 8 years. Can it sustain this level of performance? I have absolutely no idea. But I am impressed. ZWH was also surprisingly good. Though it shows the best “Worst Year” performance of the four, it had the biggest drawdown of the group, at 22.3%. That would have been a heart-stopper for me. Yet it managed to recover from that big drawdown to post pretty decent results over time. That’s a good outcome. Its total return over the period, however, lags the other two, so I would probably choose those instead. In retirement, when an income stream might be more important, ZWH might earn a place in a portfolio for some.

There’s a lot more under the hood here. Along with deciding on a US portfolio allocation percentage, an investor should consider the diversity of each fund for that US exposure. There are tax implications for US-listed vs Canadian-listed American equities in different accounts, sheltered & not. And so on. This post isn’t about any of that, it’s just an example of tailoring a portfolio to suit an investor profile that might be more, or less, risk tolerant.

What do you do for your US exposure? And be sure to let me know if you have a suggestion for a better alternative than those above.

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinion are my own, do your own due diligence & seek professional advice before investing your money.

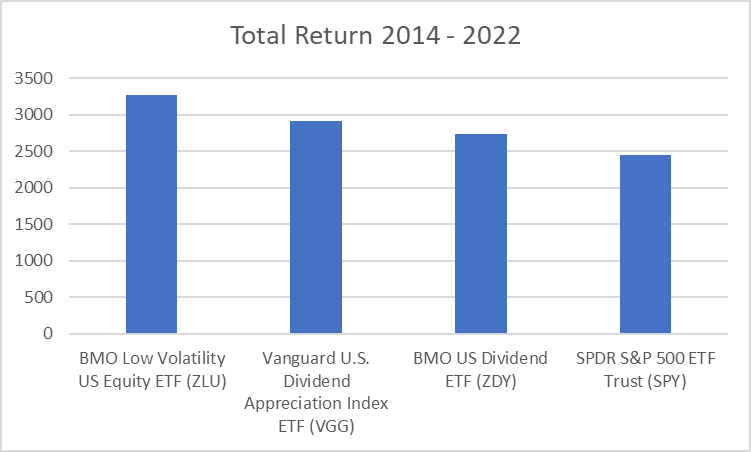

Happy New Year to all & here’s to our collective success in beating the market this year. Of course, we can’t all beat the market, we need some losers to lose money so we can be winners. But in the best tradition of reading great free advice on the internet, let me tell you that while beating the market is a big deal, it’s not that hard to do. (Make sure you don’t stop at the first chart, there is a twist to this tale! 😜)

If you’d stuck a thousand bucks into these three ETFs back at the end of 2013, & reinvested the dividends along the way, you’d have beaten “the market” with any of them. Check out the chart below, the two BMO ETFs & the Vanguard Canada ETF all beat the American index tracker. Seems like a no-brainer, eh?

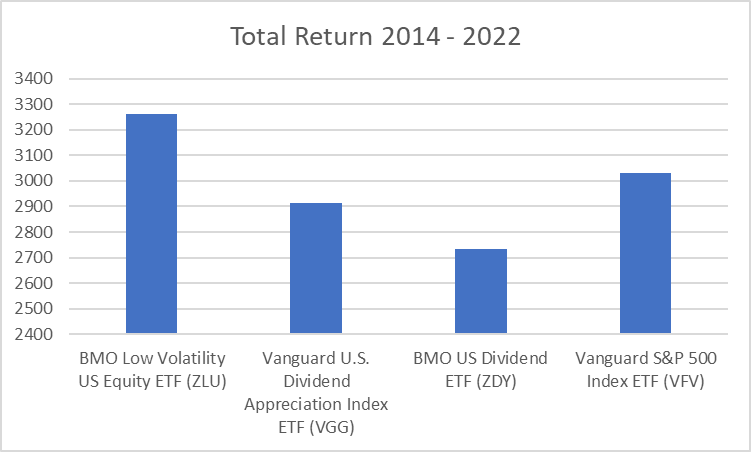

Of course, making a decision from this one chart would not be wise. And you’re seeing it on the internet, for cryin’ out loud! Instead, we’d have to do our due diligence, eh? Maybe read the marketing blurb on the fund’s website. Find a few online buddies that have invested in it & that want you to invest in it too. Ignorance, like misery, loves company. That is not doing due diligence! Now look at that same chart but, this time, with Vanguard’s VFV replacing SPY & you get this …

What’s going on here? Both SPY & VFV track the same index. Yet VFV is doing way better. It’s because we were comparing red apples to green apples in the first chart. SPY is in US dollars. Back at the start of this comparison, the Canadian dollar was strong for the first couple of years. The original investment in SPY was in US$, while the original investment in VFV was in Can$. As the Canadian dollar weakened over the years, VFV benefitted from holding US stocks, priced in US dollars. VFV is getting a numeric advantage because one US dollar is buying more loonies today. That makes VFV’s numbers bigger. But the benefit is only in the numbers, not in the value when compared to the current exchange rate. In fact, SPY would do a little better because of its lower fee structure. However, for a Canadian investor to buy SPY, there would be a currency exchange cost to consider too.

Only ZLU beat the index in both cases, so just buy that one, right? No, it’s not that simple. While all these ETFs are good, they only work as part of an overall investing strategy. They each hold differing numbers of stocks, with different sector exposures. They have different yields & costs. They are all focused on US stocks. Are they cheap or expensive relative to history & expectations? Besides, who knows what happens going forward. And 9 years is not a long time in investing cycles. Which of these you choose for part of your portfolio depends on your investing philosophy. If you don’t have a personal investing philosophy, it’ll be tougher to build an investing strategy that will work with your fears & needs. This will be different for everyone. But once you know who you are as an investor, & what you are trying to achieve, you will find it easier to invest in things that might have a better chance of delivering for you. And, sometimes, that might mean we don’t need everything we hold to beat the market all the time.

This year, as with all prior years for a long time now, my new year’s resolutions include losing weight, exercising, & saving more. Along with developing an investing philosophy that I’m comfortable with! 😜

Best of luck for 2023. I hope it’s a good one for all of us.