For a dividend investor, the answer is we never want to avoid dividends, right?

After the last post on Canadian-listed American dividend ETFs, I thought I’d provide an alternative view to one that might have suggested dividend-growth investing is the way to go.

Dividend-growth investing is very popular. I’m a fan myself. Primarily because it is a strategy that can work reasonably well for an investor with limited skills & ability to assess the potential of a stock to provide good returns. Using fewer & simpler metrics than it takes to properly evaluate a stock, it’s possible for a DIY investor to choose a portfolio of dividend-growth stocks that can perform reasonably well. And, being focused on a growing income stream, rather than on a falling share price, can help some of us ride out market downturns. The other great attraction of dividends is that as a portfolio grows, the income stream can grow &, one day, it may even match the income stream from our day job.

How cool would it be to have a portfolio that generates enough income to match your paycheque? Very cool, eh!

A retiree with a portfolio that provides a 4% yield on retirement day, might look forward to never having to sell shares. Selling shares for income can be a traumatic challenge for some retirees. And if the income stream continues to grow more than inflation, our retirees golden years might truly be golden. There’s a lot of good to be said about a portfolio of dividend-growth stocks.

But, in the world of investing, things are never simple!

Picking the right dividend-growth stocks still takes a lot of work. And it takes additional work to monitor & maintain a portfolio of individual stocks. Dividend-growth may still be a valid strategy for some. But it’s worth back-testing your stock portfolio against a dividend-growth ETF portfolio every now & then. Just to see if all the extra work produced enough extra reward. Of course the yield from such ETFs often don’t match that of a portfolio of hand-picked dividend-growth stocks. We like our bigger dividends, eh!

However, things can be different before & after retirement. And that raises some questions.

How many years ahead of retirement should we start building our dividend income stream?

Does it make sense to start early & just let the DRIP work for us ahead of retirement day?

Is it important for that income stream to grow before we retire?

But the really big question is this: should we even be focused on an income stream ahead of retirement?

Let’s take a look …

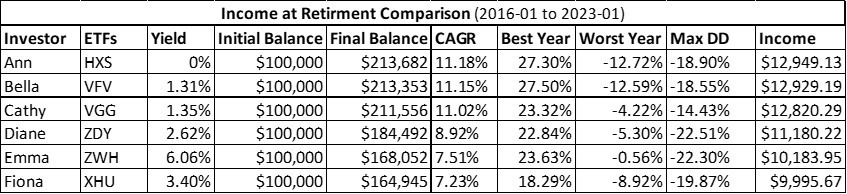

All our investors above put 100k into an ETF at the start of 2016, with a view to retiring at the end of January, 2023.

Ann & Bella are oblivious to dividends. They both followed the market index investing philosophy & went with S&P 500 Index® funds for part of their US allocation.

Ann chose Horizon’s HXS. This is a total return strategy that doesn’t pay any distribution. Unlike all the other ETFs, this one reinvests the value of the dividends inside the ETF. The income stream is zero.

Bella went with Vanguard’s VFV index fund. In this, & all other cases, distributions were automatically reinvested (the DRIP) at no extra cost.

Cathy likes the dividend-growth approach & invested in Vanguard’s VGG. She realised she might sacrifice some of the total return potential of the market, but she felt her choice was less volatile (it is, look at the Worst Year & Max DD columns) & that allowed her to sleep a little better.

Dianne was lured by the higher dividend payout of BMO’s ZDY. This ETF has a pretty good history of share price appreciation & a decent dividend growth trend. She liked that.

Emma wasn’t sure if she was into the whole FIRE thing yet but she thought that BMO’s ZWH might give her that option sooner. The juicy 6% yield from this ETF might make earlier retirement a reality for her. And the covered call strategy might offer some downside protection to boot. The Max DD is a little scary, but the worst year performance is the best of the bunch over this time period. Getting a good night’s sleep was important for Emma too.

Fiona went with a more traditional dividend approach, going with the Blackrock’s iShares® XHU offering. This is an ETF that focuses on a basket of solid, reliable, higher yielding companies in the US. A good choice for an investor who favours this approach.

Looking at the Final Balance column, I’d be pretty happy if I’d thrown a few bucks into any of these ETFs back in 2016. But what is the point of this comparison?

It’s this …

Come retirement day, we will look at things differently.

It’s not how much income was received & reinvested along the way.

It’s not how much the income stream grew prior to retirement.

It’s not about when we started to build an income stream.

It’s going to be all about the value of the portfolio on retirement day.

And how big an income stream that portfolio can buy to support our needs from that day forward.

Look at the Income column, the last one on the right. This is the income stream that would result from all the ETFs being sold off on retirement day to buy ZWH, the highest yielding ETF. The biggest income stream can be had by selling the portfolio that gave the best total return. And then buying the ETF with the greatest distribution, in this case ZWH. There is a 30% spread here, that’s significant.

Notice that in most cases, the higher yielding funds tend to have lower total return over time. That might not always be the case & it might not be the case going forward. Not even amongst this batch of ETFs. Doing your own due diligence, as always, is important.

But, from a pure numbers perspective, it matters less what happens with dividends during the accumulation years. It only matters that the portfolio grows. As much as possible. The bigger the portfolio, the bigger an income stream it can buy on retirement day. In this example, how much the income stream grew during accumulation didn’t matter. Having a bigger yield on cost didn’t matter. The only thing that mattered was that a bigger portfolio bought a bigger income stream on retirement day. For simplicity & to maximise return, all investments were considered to be inside a tax-sheltered account. There are other implications, not covered here, for selecting ETFs like this in a non-sheltered account.

Emotionally & numerically, there are many reasons that investors choose to invest differently. Seeking solutions with lower volatility, the reassurance of a growing income stream, avoiding the need to sell shares, & so on, all factor in to individual choices. All these are all important considerations, for sure. But the message here is not that we all need to abandon our chosen strategy in favour of some other promoted strategy. It’s more about giving some thought to strategies that differ from our current path. Despite the reassurances we get from like-minded investors in our favourite social media groups, it can be useful to think differently about things from time to time. We shouldn’t fall in love with one particular strategy & block out all information that conflicts with that. It might be worth taking some time to learn about different perspectives & different strategies. Keep an open mind.

By the way, I’m not suggesting that you buy any of the ETFs here. Nor am I suggesting that everything gets dumped on retirement day for one high-yielding ETF. This is just an example to illustrate why we might want to think differently about our approach from time to time. It’s just as a valid to consider switching to a basket of individual, higher-yielding, dividend-growth stocks on retirement day, for example. Or sticking the proceeds into a portfolio of your favourite high-yield funds. Do whatever floats your boat for an income stream. Believe it or not, some will stick with the growth solution that got them there & sell shares for income. But regardless of approach you choose during the accumulation years, whatever you choose to do in retirement will probably work better with a bigger portfolio. 😜

So how do you accumulate?

Important – this is not investing, tax or legal advice, it is for entertainment & educational purposes only. Opinion are my own, do your own due diligence & seek professional advice before investing your money.